We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

The actual argument being made is that British actors, tax breaks, directors, scriptwriters, lovely Cotswold villages (and in the case of Bridgerton, the street outside my flat) are just such wonderful places to film, film with, that prices are rising. Therefore we’ve got to subsidise all this.

The only reason we listen to fuckwits like this is because they’re pretty. Now, honestly, hands up. Who has ever known a pretty bird, handsome man, who can actually think? Even, actually has the base data to be able to think with?

No, no, it’s not that the leavening of IQ and looks equals out over genes. Quite the opposite. Dullards in the sense of actual cretins and morons tend not to look good either. But the good looking have never had to think now, have they? So, they don’t.

– Tim Worstall

Democracy tends towards protectionism when those harmed by free trade are numerous enough to count. But democracy also demands cheap goods. No one has yet squared that circle.

– Robert Tombs

What’s more, the imposition of punitive tariffs on poorer countries like Vietnam will simply impoverish rather than improve the potential importing power of these countries. Disrupting the economic development of poorer countries isn’t going to improve the chances of selling to them.

The irony is brutal. Trump’s fixation with trade-deficit “offenders” is punishing the very nations that could one day erase those deficits through development and prosperity. US consumers, businesses, and economic growth will all suffer as a result of the US president’s inability to grasp this elementary logic. There seems to be just one long-term strategy behind all this: unleash populism for immediate electoral returns, blame someone else for the problems that populism inevitably causes, and let someone else deal with the long-term consequences.

– Robert Johnson

“Perhaps the greatest paradox of all is that parts of the Maga movement are embracing a form of Right-wing wokery, with their own dark conspiracy theories, cult of victimhood, identity politics, denial of reality, moral grandstanding, hypersensitivity and purity tests.

“In this vein, whingeing about trade deficits deserves to be dismissed as critical trade theory’, as Trumpian corollary of critical race theory: it postulates, nonsensically, that any shortfall must be caused by unfair practices, oppression or historic injustice. The ‘woke Right,’ a term coined by James Lindsay, is almost as much of a turn-off as the original Left-wing variety.”

– Allister Heath, Daily Telegraph (£)

He gives Mr Trump high marks on taking the fight vs DEI, some of the DOGE cuts (with a few caveats), and on energy policy (which in my view is Trump’s ace in the hole). But the broader point Heath makes about where he thinks Trump/Maga is losing it, including this nifty term of Heath’s, “critical trade theory”, is absolutely spot-on. It is, in my view, one of the big blinds spots of today’s populist Right and threatens to undo the good things that a Trump 2.0 might achieve, which would be bad not just for the US, but the West in general. As Heath goes on to write (and remember, he’s a pro-Brexit, free market chap, and not some obdurate Never Trumper), a course correction is needed. And Trump is not incapable of it.

As you can imagine, there have been a lot of attempts to make sense of what Mr Trump is trying to do about tariffs. As of the time of my writing this, the dollar is coming under pressure, Mr Trump appears to be ratcheting up the tariff war with China to even higher levels, and there are signs that a few of his allies are getting nervous (seriously, how on earth can he have people working in his government such as Elon Musk and Peter Navarro who talk to each other in this way?)

One way to think about the the US/rest of world imbalances is that this is about production and consumption. In various ways, countries such as Germany, Japan and China produce a lot, and tend to be careful on how much they consume; on the flipside, the US loves to consume. As Joseph Sternberg in the Wall Street Journal puts it:

The core of Intellectual Trumpism runs as follows: The global economy is characterized by large, policy-induced imbalances in both trade and capital flows. These are caused at root by the decisions of some large economies—Germany, Japan and especially China are the usual suspects—to subsidize production by suppressing consumption in their domestic economies. This creates “surplus” output that they foist on the U.S.

This view isn’t wrong, so far as it goes. Those economies and others historically deployed a range of policy tools to boost exports. In China, the most egregious manifestations are direct subsidies for exporting companies. Less visible to foreign eyes is the financial repression: the deliberate suppression of domestic interest rates and political control of credit to subsidize businesses (which benefit from cheap borrowing) at the expense of consumers (who receive less income from their saving and investment). Such policies can take many forms. In Germany, extensive subsidies shield large companies—meaning exporters—from the worst energy-price consequences of Berlin’s dumb net-zero climate policies. Households pay full freight for electricity.

This is an interesting point about the control of credit and yes, Net Zero, intersecting in ways that suppress consumption and encourage production, much of which has to go overseas – to places like the US.

Sternberg continues:

Because other economies under-consume, the argument runs, they accumulate excess savings. They recycle these savings into the U.S., where we transform foreign claims (in the form of equity investments or purchases of American debt) into consumption of the foreign country’s excess production. Hey presto, a trade deficit.

An oddity of this argument is how little agency the U.S. is said to exercise. Once Washington had made the first mistake of opening our economy via tariff reductions and the free flow of capital, it was off to the races.

The truth is much more complex, and politically challenging: While some other economies suppress domestic consumption and subsidize export production, Americans choose to do almost exactly the opposite. Through political choices such as suppressing energy production and distribution, or permitting red tape and the like, or any number of other policy foibles, we make it much harder than it otherwise would be to produce things in the U.S. Meanwhile, you can’t take a step in America without tripping over a consumption subsidy.

So what has the US been doing to encourage consumption?

To cite a few: Fannie Mae and Freddie Mac stimulate overconsumption of housing. Subsidized student loans stimulate overconsumption of higher education (which, given the poor lifetime earnings prospects of many degrees, should indeed be understood as consumption rather than as an investment in human capital). The earned-income tax credit creates complex distortions that at the margin subsidize consumption while discouraging additional productive work.

Most glaring, though, are our entitlements. Social Security, Medicare and Medicaid, not to mention a raft of other benefit programs, funnel vast quantities of money into consumption. The trick here is that we’re able to finance these via chronic fiscal deficits funded by foreign investors, meaning at the margin Americans borrow from the rest of the world at ultralow interest rates and funnel the cash into consumption at home.

And as the writer says, the “root-cause” solution to the trade deficit issue, to the extent that it is a problem that governments should address, is to rebalance – get rid of consumption subsidies and stop penalising production. That means, for instance, rolling back regulations, zoning laws, etc. (To the limited extent that this is being done by Trump, that is a mark in his favour.)

Some elements of such an agenda can be popular, as Mr. Trump is discovering with his deregulation and cheaper-energy drives. But the entitlement half is a minefield. Republicans are reluctant even about dialing back Medicaid benefits for able-bodied working-age people. The last time anyone tried to reform Social Security, President George W. Bush backed allowing a portion of payroll tax payments to flow into individual investment accounts. The existing system creates a consumption subsidy by transforming tax payments into transfers to recipients; the reform would have created a form of investment subsidy. That bit of good sense degenerated into a traumatic political fiasco for the GOP.

This the key. Social Security and other big entitlement programmes in the US are, as they are in the UK and much of the West, popular with ordinary voters; and the voters who switched from the Democrats to Republicans in 2016 and 2024 aren’t going to be happy to see these programmes reformed or reduced. It is therefore easy to see why tariffs are a tempting technique – it is easier to go on about those naughty, over-producing Asians and Germans as being at fault, rather than because incentives are structured as they are.

Sternberg concludes:

Note that the end result [of tariffs] is in one way the same as entitlement reform: less U.S. consumption, only via the demand suppression of higher import prices. But beyond that, the two policies diverge—and not to Intellectual Trumpism’s advantage. Among many other problems, protectionism risks depressing domestic production, a warning emerging from industries across America whose supply chains are imperiled by tariffs. It certainly doesn’t help domestic productivity. Entitlement reform, by contrast, tends to be an enormous supply-side spur to future economic growth that benefits households as inflation-adjusted wages rise.

The problem, however, is that entitlement reform is very hard to do, politically. There are some things that will also be politically tough: not everyone likes deregulation, given how occupational licensing and so on often shields vested interests. (Think of how the London mayor tried to hit Uber, at the urging of the traditional taxi sector, a few years ago.) Zoning laws are a problem but they are also supported by people who want to protect the value of their properties, as they see them, and so on. In certain countries, the planning system is so convoluted that it is a major brake on production. Fixing all this takes political will and the risk of antagonising vested interests.

As Matthew Lynn, a columnist writing in the Sunday Telegraph (£) puts it, the compulsion on car firms to build more electric vehicles (EVs), on pain of large fines, was already causing great damage to the UK and European economy. With the US now imposing blanket 25% tariffs on car imports from the UK, the Net Zero obsession is suicidal for the UK-based car industry, home to brands such as Jaguar Landrover, which has just paused shipments to the US:

“It would be ridiculous for the Government to start fining the car companies for not selling enough cars that no one really wants at the same time as the Trump administration is hitting them with huge new levies in their main export market. None of the car companies is in exactly great shape to start with. The combination may well prove fatal.

The [UK] government should announce an immediate one-year suspension of the EV target, and then start a consultation on postponing it for another five or even 10 years. If it was scrapped immediately no one would miss it.”

Tens of thousands of car workers could lose their jobs, unless there is a drastic change in policy in the UK – never mind what the Trump administration chooses to do – and they live in those famed “Red Wall” seats that the insurgent new party, Reform, is targeting at the next General Election.

[a] trade imbalance is not an inherently bad thing. it can be a very good thing, a beneficial thing. this idea that if we buy $50bn more goods from kermeowistan every year than they buy from us that it implies that they are somehow “taking advantage” or this this is “unstainable” or negative is flatly false. it’s actually ridiculous. it ignores complex trade flows and balancing factors like “capital flows.”

people really seem to struggle with this, but it’s not that difficult. you’ll will have a large lifetime trade deficit with the grocery store. you will buy much from them. they will buy nothing from you. is this a problem for you? is it unsustainable? most people seem to sustain this beneficial grocery trade their whole lives.

why is it any different if it crosses a border or gets aggregated by nation? (spoiler alert, it’s not)

you’ll likely run a lifetime trade deficit with many countries too. you buy a BMW. that’s a deficit to germany. you run a restaurant in toledo. you have no german customers. does this fact harm you in some way? did germany take advantage of you? would it be better for you if we imposed a tax that made that BMW 25% more expensive? no, and if we do, it might create automotive jobs in the US, but the cost to do so is YOUR choice and your budget.

– El Gato Malo

Follow the link, read the whole thing.

Well, he went ahead and did it. In a ceremony outside the White House, Donald Trump unveiled a list of tariffs on countries, on “friend and foe”, starting with a minimum of 10% (the UK, which is now outside the European Union, was hit with the 10% rate, while the EU was hit with double that amount). In general I see this as a bad day for the US and world economy for all the sort of reasons I have laid out.

This will not adjust the worldview of the red hat wearers, but I wonder has it ever occurred to Mr Trump’s fans that his arguments, when adjusted for a bit of rhetoric, are more or less leftist stuff from the 1990s?

Ernest Benn was the uncle of Tony Benn and great-uncle of Hilary Benn. Luckily for us he was the black sheep of the family and pursued a career in business before becoming one of the “great and the good”. And then he decided he didn’t want to be great or good any more, founding the Society for Individual Freedom. As I understand it the Libertarian Alliance – who most here will be familiar with – emerged from that association.

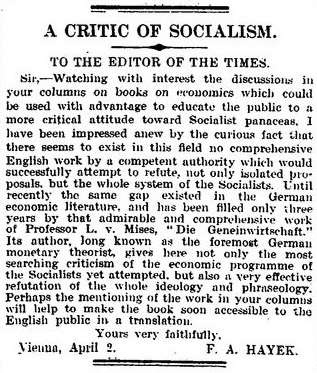

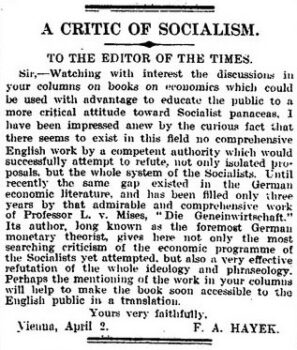

A hundred years ago Benn was compiling a list of good economics books which – seemingly unbelievably – The Times published. It includes – as you might expect – Smith, Bastiat and Mill and – as you might not expect – Spencer and Smiles. It also includes Henry Ford – presumably before he started blaming the Jews for everything. But there is one book that’s missing. Luckily a young Austrian is on the case.

The Times, Tuesday, 14 April 1925 [I hope this is legible. It’s a bit blurred on my computer but the original is fine. The list is totally blurred if I try to include it inline with the post. All very odd.]

Elliot Keck (who he?) had this recent excellently sharp item over at CapX:

It can be infuriating making the case for free markets. Too much time has to be spent batting away obviously terrible, tried-and-failed ideas. Proposals for a wealth tax are just the latest iteration requiring many a wall to be bashed with many a head. Just in the last few days, a group called ‘Patriotic Millionaires’ has urged Rachel Reeves to consider a ‘simple way’ to grow the economy with a tax of 2% on wealth over £10 million per year. A recent piece in the New Statesman concluded that a wealth tax wouldn’t be straightforward, but it could work. The new director of the Institute for Fiscal Studies has also called for a one-off wealth tax.

This is mad. As a TaxPayers’ Alliance study of wealth taxes has demonstrated, they’ve failed everywhere they’ve been tried. When Labour considered one in the 1970s, they concluded it would be unworkable, despite capital being far less mobile then than it is today.

We are already seeing the wealthy flee at a shocking rate (just look at the Adam Smith Institute’s millionaire tracker), forced abroad by changes to non-dom rules, punitive marginal tax rates, shoddy public services, increasing crime and the imposition of VAT on private schools, to name just a few incentives. When this is pointed out to proponents of wealth taxes, as I recently found on LBC, the response is not to dispute the problem but to bemoan the fact that every time the rich are asked to pay their ‘fair share’, they throw their toys out the pram and flee.

Yet now those who have the temerity to be affluent are being told to cough up to clean up the almighty mess made by our political class. It’s yet another reason for the wealthy to line up for the last chopper out of Saigon. Rather than criticising those who leave, we should increasingly be thanking those who choose to stay.

“America doesn’t make anything anymore” is a powerful talking point, but it’s false. We make plenty, including some of the most complex, high-valued goods in the world, from aircraft to pharmaceuticals to advanced electronics. Our workers don’t make many T-shirts or toasters; other countries can do it more cheaply. And the more successfully we produce and export advanced machinery, the more foreign goods we can afford to import. America’s industrial base is not collapsing. It’s evolving—becoming more productive, more specialized, and more capital-intensive. Protectionism won’t bring back the past or revive old jobs. It will just make the future more expensive and shift workers into lower-paying jobs.

– Veronique de Rugy, Reason magazine.

Lest any Trump admirers get all upset about my posting this quotation it is worth pointing out that there is plenty of protectionist guff on my side of the Atlantic as well. The EU has its Customs Union – the aspects of the bloc that I like the least – and it is described in typically bureaucratic fashion, here. This article in the Financial Times contains the claim that the EU is not as comprehensive in its “protective shields” as the US, Canada and Australia. That said, free trade in general terms is in global retreat, unfortunately, and not simply under the Trump administration – previous US governments were hardly much better, although that is not setting the bar very high.

I have jousted a bit in the comments on previous threads with those claiming that tariffs are necessary, for various (and to my mind, fallacious and often self-contradictory reasons): to “protect jobs”; national security and diversification of supply; as a club to hit supposedly foolish and oppressive other countries; to raise taxes and shift away from income taxes, or that comparative advantage on the David Ricardo model does not work if you allow cross-border capital flows. All the arguments are, in my view, flawed and in some cases, just plain wrong. (Here is a good summary of the arguments contra protectionism.)

As it is used a lot these days, here’s a good take-down, from the Hoover Institution, of the “national security” argument for tariffs. I can also recommend a new book, Free Trade In The 21s Century, a collection of essays by folk from the political, business and economics world. It is a big read, but good to immerse in if you want to delve into the arguments.

What I see playing out today in the US – and at times in Europe – is the way that, since the end of the Cold War and the supposed triumph of free market ideas in the subsequent 20-plus years, the argument was not made with sufficient force and the benefits not adequately spelled out. So here we are. And one big problem is that what Austrian economist Joseph Schumpeter called the “creative destruction” of capitalism meant that the supposed losers of all this commotion, such as car workers in the UK West Midlands or the US “rust belt” did not get, as far as they could tell, much immediate uplift from the greater overall prosperity that open trade brought. Telling them to “learn to code” just riled them up. (Explaining to an unemployed coal miner or machine tool operator that they should learn a very different skill is difficult, at any age, but particularly if the argument comes from a politician who appears to have never had a real job.) And this, it seems to me, is the fundamental issue: how can a culture of adaptability and can-do attitudes be fostered in a world of constant and at times, disturbing change? (Robert Tracinski makes a good attempt to do so, here.) Because if that does not happen, the populists of the left and the right, whether a Trump, a William Jennings Bryan, etc, will energetically seek to fill the market void. (HL Mencken magnificently destroyed Bryan, who was an opponent of gold-backed money and held many other terrible views that are, I fear, still popular in certain quarters.)

This book, Capitalism In America, from a few years ago by journalist Adrian Wooldridge and former Federal Reserve chairman, jazz musician and economist Alan Greenspan (full disclosure: I have met both of them), gives a good overview of the rise and fall and then rise of arguments about free trade, globalisation, the problems with how the losers from disruption can demand destructive changes, and more. If advocates of free trade like me cannot explain all of this, then the protectionist argument will gain ground, to calamitous effect.

Defining the benefit of spending as who gets the money rather than what gets bought is economic insanity. We might have a little insight there as to why government control of the economy ends up impoverishing.

– Tim Worstall

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|