We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

Germane to Michael Jennings’ post below pertaining to Prince’s declaration that the “Internet is completely over”, I had a brief conversation with a decidedly winsome 20-something young lady, elegant yet edgy (she was a cut glass accented thoroughbred Sloane Ranger wearing ‘All Saints’). She was sitting in a sandwich shop in a well-heeled part of town… expensive Apple laptop open as she availed herself of the free WiFi whilst having luncheon…

The following really happened, serious, not joking.

Samizdata Illuminatus “Did you read that Prince thinks the ‘Internet is completely over”? He refuses to release any of his music on it at all”

20-Something-Young-Lady “Really? Umm… I did not even know he was a musician.”

SI “Well, yes…he is. He is one of the great guitarists of our time.”

20-S-Y-L “Hah, that’s funny! I cannot picture that old foggy playing a guitar! I thought he just spent his time playing polo, messing with architects and hugging trees…”

SI “No, no, no, not Prince Charles… ”

20-S-Y-L “Prince William? No, I am sure you must mean Harry! Oooo! Yummy Harry with a guitar!”

SI “No, the American musician called ‘Prince’.”

20-S-Y-L “Oh, I see. And this chap calls himself ‘Prince’? That’s hilarious!”

SI “He used to call himself ‘Squiggle’.”

20-S-Y-L “I’m sure I’ve never heard of him.”

SI “I suddenly feel very… old’.”

20-S-Y-L “I’ll download something of his off Bit Torrent and see if he’s any good.”

I do not believe she immediately grasped the sheer transcendent irony of the moment.

Apologies to Samzidata readers if you have already seen this, but I had not, and boy, this is just gooooooood.

Contrary to what most people had assumed, banking in the United States had been highly stable in the decades before deposit insurance. Of course, depositors were concerned about their safety, but this made them cautious in whom they banked with. They demanded reassurance from their banks, and the banks gave it to them. Pressure from depositors forced the banks to be conservative, to lend carefully, to keep their leverage ratios low, and to disclose their broad positions. The bankers themselves were conservative even in their dress, but this was itself reassuring, and the solid architecture of the banks’ offices reinforced the notion that they were pillars of the community with solid roots in it. The key to banking was maintaining the confidence of depositors and not taking that confidence for granted.

Before deposit insurance, a bank that took too many risks would eventually undo itself. It would do well for a while, increasing market share and generating better shareholder returns than the fuddy-duddy banks, which would feel the pressure. However, come the inevitable downturn, the cowboy bank would experience heavy losses on its questionable lending, liquidity would tighten, and a point would come where the frightened depositors would run for their money: the cowboy would be literally run out of business. These occasional crises were unpleasant, but good for the long-term health and even stability of the system: the runs would expel the cowboys from the system and give a salutary reminder to those who survived. The system itself was rarely seriously at threat, because the depositors would redeposit their funds with the safe banks. There would typically be a flight to quality, a transferring of funds within the system, rather than a run on or threat to the system as a whole. Thus, it was the threat of a run that kept the bankers in line.

Once you introduce deposit insurance the situation changes profoundly. Deposit insurance allows the bankers to take their depositors’ confidence for granted. This takes the pressure off the bankers, who can now safely increase both their lending risks and their leverage ratios, thereby increasing returns to their shareholders (or, in modem Wall Street, to themselves). For their part, the depositors are no longer concerned with the risks their banks are taking, but only with the rates they get on their deposits. Consequently, deposit insurance subsidizes risk-taking, so leading to excess risk-taking with the deposit insurance agency and, ultimately, the taxpayer, picking up the tab.

Nor does the damage end there. With deposit insurance, there is no longer any run to fear and even the most insolvent banks following the most unsound “shoot to the moon” investments can now remain in business indefinitely, attracting more funds and staying in business by merely raising deposit interest rates. The process of competition then becomes utterly subverted: instead of allowing the conservative banks to drive out the cowboys, even if it takes a little time, the process of competition now rewards the cowboys and penalizes the good banks. It therefore pays to become a cowboy and, eventually, all banks do.

– From Alchemists of Loss by Kevin Dowd and Martin Hutchinson (pp. 271-2). Pictures of the two authors here, taken at the launch of the book last Wednesday evening at the Institute of Economic Affairs.

As I have seen before, a lot of political news coverage in the UK (and in the US, for that matter) rather resembles sports coverage, if without the tone of hysteria covering the media’s reporting on England’s World Cup horror show. For instance, over at the Spectator’s Coffee House blog on the issue of public spending cuts, it goes into a lot of the arguments about who said X or Y about cutting A or B. In fairness, the Coffee House crew are pretty good at teasing out the statistics – Spectator editor Fraser Nelson has been excellent in hammering the former government over its debt – but there is something a bit missing from its analysis. And that is this: the scale of the shift that we might see from public sector jobs to private sector. If is true that hundreds of thousands of public sector jobs are to go, and the private sector is going to be encouraged to pick up the slack by new job creation, that is surely good news.

We are not admirers of Cameron’s style of Conservatism here at Samizdata (that’s putting it mildly, Ed), but I’ll give him and his finance minister credit if, at the end of the current parliament, there has been a significant shift away from the state and towards the private sector. We libertarian ideologues are hard to please, but such a shift will be pretty tough to pull off. If it means we have to put up with a certain amount of political BS along the route, I don’t especially mind. It is the general direction that counts.

Update: Guido Fawkes points out that certain leftist publications, reliant on public sector job ads, such as with the Guardian, have an obvious reason to fear the axe. It’s not a bug, it’s a feature!

Basic logic is something that Mr Richard Murphy, wonderfully flayed by the indefatigable Tim Worstall, is blissfully unaware of. As Tim points out, Murphy reckons we can use inflation to somehow “wash” out massive debt (by shafting savers and others on a fixed income) while he also vents about the terrible plight of pensioners and the need to protect them.

It might be easier to deal with Richard Murphy in the same way that you might an old, very ill dog. Don’t worry, Richard, there would be no pain.

This posting is going to have to be of a more than usually interrogative sort, since I am more than usually ignorant of that whereof I blog, and which I will now copy and paste:

Certainly, on my travels, I’m going to be wary of accepting euro notes with serial numbers that are prefixed with the letters Y (coming from Greece) or M (from Portugal).

I shall also strongly steer clear of notes with the serial numbers starting G (Cyprus), S (Italy), V (Spain), T (Ireland) and F (Malta).

This might sound as if I’m being ridiculously alarmist, but you cannot be too careful.

However, other euro notes should be reasonably safe.

These include those marked Z (Belgium), U (France), l (Finland) and H (Slovenia). As for those with serial numbers beginning with X (Germany), P (the Netherlands) and N (Austria), they can all be used with total confidence.

Is this common knowledge? Am I the last person in Europe to hear about this? I shouldn’t be surprised. You can tell which country printed which Euro. Well, well. Who knew? Who, even now, knows?

The above quoted text is from a Daily Mail piece by Peter Oborne (linked to by Instapundit) about the various economic disasters the world faces. One of which is the melt-down of the Euro.

My big question, aside from wondering who else does or does not know this, is: supposing lots of people do know this, or get to know it, does it not provide a mechanism by means of which mere people might hasten the collapse of the more dubious EUrozone economies, by demanding, when being paid in actual money, to be paid only in Euros printed by the undubious countries?

Perhaps the answer might go: but making such judgments would be, in EUrope, illegal. Maybe so, but that won’t stop a black market making minute comparisons between differently lettered Euros, nor will it stop tourists in other parts of the world, planning their EUropean trips, demanding, once they hear such stories, to receive only the kinds of Euros that they would like. They could, for instance, refuse to accept the wrong kind of Euros, or, if given a mixture of good Euros and bad Euros, sort out the good from the bad and swap the bad ones back for pounds, or dollars, or whatever.

The wrong kinds of Euro notes, from the dubious countries, could soon be treated exactly as if they were forgeries, could they not? The big difference being that these forgeries will be easier to spot.

So, the much prophesied melt-down of the Euro can now be accelerated in a much more discriminating way than merely by people judging that the Euro as a whole will soon be disappearing down the toilet. We will all be able to decide – many may soon be forced to decide – which Euros will descend toilet-wards first. Won’t we? Can’t we? Now? I realise that there is more to money than mere bank notes. But if stories like those sketched above were to start circulating …

Has Oborne got his facts right about this? And if he has, do my supplementary questions also make any sense? As I say, this is all completely new to me, so I could soon, after the first few responses, be wishing that I’d never even asked.

In the United States one of the biggest exercises in false consciousness the world has ever seen – people gathering in their millions to lobby unwittingly for a smaller share of the nation’s wealth

The Guardian’s George Monbiot is talking about the US Tea Party Movement.

Which is it, do you think? Has nobody ever told him about the fixed quantity of wealth fallacy, or does he just enjoy winding people like me up?

“As you march grimly forward through the detritus of economic debate, with a Sturmgewehr 90 assault rifle and fixed bayonet gripped firmly in your hand, thousands of blind Keynesian moles will leap up from deep dark holes in the mud to bite your ankles.”

Andy Duncan. Like Andy, I have read Thomas E. Woods’ Meltdown book and I wrote out some thoughts about it here. And here.

Glad to see Andy is writing away. Old Samizdata hands may remember he used to scribble for us occasionally.

Steve Baker MP’s maiden speech.

Tried to finish a longer piece involving that link, but failed. There’s the link anyway. Now rushing out to a meeting organised by the very organisation that published that blog posting. Such is life.

The ultimate cause of the problem with the banks was indeed chronic government interference, in the form of implicit and explicit guarantees supplied to them free of charge, which hopelessly weakened the entire industry. Reserve ratios – the percentage of deposited cash which is actually retained by the bank rather than lent out – has fallen from over 50% in the 19th century to 2-3% today (or a negative percentage in Northern Rock’s case). That could not have happened in a free market, at least not on an industry-wide scale; nobody would lend to a bank if it tried to take on that much leverage without a government guarantee.

The banking industry had been rendered so unstable by government intervention that it was only a matter of time before it had a crisis, and the crisis could have been brought about by any number of proximate causes. Unfortunately most commentators blame the proximate causes, the particular individuals who happened to be involved at the time, and “free markets”.

In a free market, firms fail from time to time; they aren’t bailed out, people don’t expect them to be bailed out, people arrange their affairs accordingly and so the failure of one firm doesn’t bring down an industry or an economy. Banks were a long way from being a free market.

– “Some Guy” (that’s what he calls himself) commenting on the Bishop Hill piece also linked to below by Johnathan Pearce in connection with Matt Ridley’s inglorious career as a banker

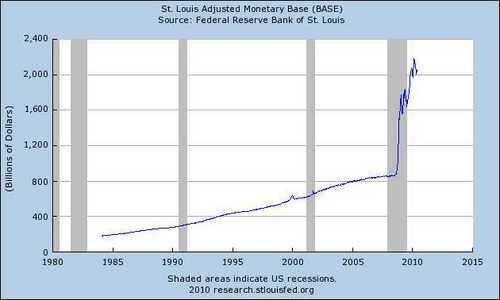

This is a quick thumbnail of money supply for those of you having trouble finding understanding in the tsunami of Keynesian Kool-Aid coming from our ‘betters’.

On October 3rd of 2008, Republicrats and Democans responded to the failure of Lehman Brothers, bankruptcy of Bear Stearns, incipient collapse of AIG Insurance, threatened insolvency of other major financial institutions, and general panic in the financial community, by passing Public Law 110-343. This law contained two basic sections. The most infamous brought us the first of the ‘TARP–ulus‘ genre. But a very important offsetting function was contained in another place in that same law that is known as the Emergency Economic Stabilization Act of 2008. Way down in the fine print, it authorized the Federal Reserve Bank to begin immediately paying banks to not loan out money. That was not their exact choice of words. In fact, read Section 128 where they did it and it is almost impossible to tell what exactly they were doing.

Three days later on October 6th of 2008, the Federal Reserve Bank announced it would begin paying banks to not lend money. Again, not their exact choice of words.

Within less than a month the Federal Reserve Bank began discreetly ‘monetizing’ by purchasing Fannie and Freddie debt.

By March of 2009, attempts at discretion fell by the wayside and the Federal Reserve began buying US Treasurys outright. Put simply this means that the Federal Reserve began ‘printing’ money and giving it to the United States Treasury to spend.

During this period of time (from September 2008 through current) the St Louis Adjusted Monetary Base went up by approximately 1 trillion dollars.

Since that time, consumer prices have anomalously trended flat (click ‘view data’ for specifics) in spite of the adjusted monetary base more than doubling. How can this be? → Continue reading: Money supply, the stimulus & where is the inflation?

A superb video from the TaxPayers’ Alliance asks…

… how long do you work for the tax man?

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|