We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

Too bad there already is an SQoTD for today, but here’s a classic bit I’ll copy and past for you anyway:

We are almost getting to the situation where we will be seeing unemployed environmentalists walking the streets. As with unemployed actors who describe themselves as “between jobs”, one might expect them to admit to being “between scares”.

That’s the EU Referendum man, Richard North, ruminating about how the environmental debate is now going quiet, and about how the forces of darkness are now going to have to find themselves a different line of bullshit to work with. “Biodiversity” won’t nearly suffice. How true. Although, as he’d be the first to remind us (I found that link in this), “climate” money is still being thrown around like there’s no tomorrow, and if that carries on there probably won’t be. Anyway … as I was saying. Between scares.

That phrase could really get around. It deserves to.

I know we keep banging on here about Steve Baker MP, but he really is excellent.

The thing about Baker is that he doesn’t just say the uncompromisingly libertarian things that he does say about economics and economic policy, and about, to quote the title of his talk, honest money and the future of banking. He is willing to be immortalised on video saying them, and therefore potentially to be heard saying them everywhere on earth. Amazing. Truly amazing.

This performance lasts just over forty minutes. I urge you to make the time to look at it and listen to it. If, like me, you have any sort of drum handy, I also urge you to do some banging on about it yourself.

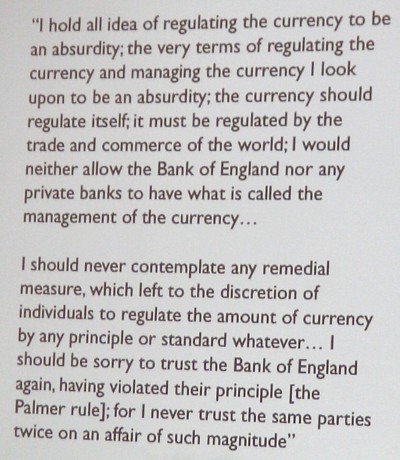

– Richard Cobden (1804-1865), quoted at the Cobden Centre website. Quoted again by Steven Baker MP at the end of his presentation this morning to the Libertarian Alliance, and featured in his final slide, of which the above is my somewhat wonky photo.

Here:

In a fascinating 36 minute interview, Cobden Centre Radio’s very own Brian Micklethwait speaks to James Tyler, the Chief Executive of Tyler Capital and a member of our Cobden Centre advisory board.

I’ll surely have more to say about this, but busy day today. So suffice it to say, for now, click on this to listen to the mp3, or follow the top link to find it as a podcast.

My main general impression of James Tyler was what a good and thoughtful person he is, very much his own man in how he thinks about things and goes about things, yet in no way scornful of or unsympathetic towards others who take the road more travelled. If the propaganda fence to be got over is that Austrian economics, once you’ve been told about it by your resident lefty, is an excuse for billionaires to piss on everyone, then a man like Tyler is just the sort to get you thinking that it’s a whole lot better and more intelligent than that.

His central point was that nobody should have the kind of power over economic life that our current powers that be (“crony capitalism”) do now have.

Incoming from Sam Bowman of the Cobden Centre (and also the Research Manager and Blogmeister at the Adam Smith Institute – most recent blog posting here):

This Thursday 28th October, the world’s leading economist of the Austrian school – Jésus Huerta de Soto – will be giving the first annual Hayek Lecture on the topic “Financial Crisis and Economic Recession”. The lecture is a great chance to hear about the Austrian Business Cycle Theory from its leading living theorist. It’s free, no advance tickets are needed. It starts at 6:30pm and full details are available here.

That event has already been flagged up (although somewhat imperfectly!) here. The Cobden Centre head honchos are hoping for a good-to-bursting type turnout, to keep the buzz they are already creating buzzing along and buzzier. So if you can just show up, do. No compelling need to listen to everything that carefully, or not first time around, because unless things go badly wrong the event will be recorded. I will be going, and I expect to learn a lot.

And there’s more:

A conference is being put on in London on Saturday 13th and Sunday 14th of November by the Positive Money campaign. The conference is not Austrian – there will be speakers from a range of intellectual viewpoints – but it will focus on the issues of money and banking and will have lectures from several Cobden Centre board members, including Toby Baxendale, James Tyler and Steve Baker MP. Full details are available here.

One of the things I most like about the Cobden Centre is how they cooperate so enthusiastically and helpfully with other groups which have broadly (rather than merely narrowly) similar agendas, that latter event being typical of this mind-fix.

This article by one of the Home Depot founders has been out for a few days, but I thought it would be good to put it up as it communicates, with a sort of barely suppressed rage, how businessfolk in the US feel patronised and insulted by the sort of policymakers in Washington, obviously starting with Obama.

And I would happily wager that there are a lot of business people who feel pretty much the same way about the UK, as well. I just wish we would have more entrepreneurs making these kind of comments.

Probably the most devastating take-down yet of the economist and leftist news columnist I have ever read. The man’s credibility is in total ruins. The stuff at the end about the housing bubble is the killer. Read the whole thing.

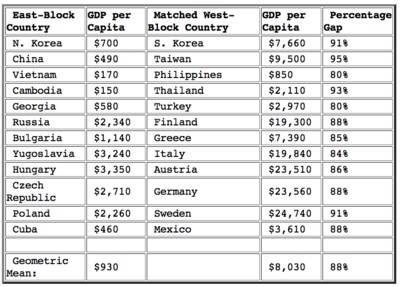

When in my teens, in the 1960s, I wondered what rules were best for governing the world, and the nations in the world. Comparisons like this (featured by Tim Worstall at the ASI blog today, he having come upon it here) helped me to decide:

As Tim Worstall notes:

[T]he countries are matched as to rough starting point before the communist armies marched, matched roughly as to culture and so on, and yet after that series of communist experiments we see the same result everywhere.

Exactly. It was the matching of like (to start with) with like that was most telling. And before 1990, we also had the damning comparison between East and West Germany (very near to my English home) to contemplate.

So, said contemporaries who were drawing more nearly opposite conclusions, you want sweatshops like they have in South East Asia? With growing confidence, I learned to say: yes. If people in South East Asia now have sweatshops, that’s a pity. They must be very poor. But how will shutting down those sweatshops make them any less poor? You’re saying poor with hope of escape is worse than poor with no hope at all. That sounds downright wicked to me.

That time proved me, and all who argued as I did, right was one of the big reasons for communism collapsing where it did collapse, and trying to insert capitalism into itself where it did not.

Some libertarians now live in dread of a time when such comparisons will no longer be possible, because the entire world will be equally stagnant, and nobody except them will be able to see this. Some people are determined to be miserable.

El socialismo es contra la prosperidad.

– Instapundit flags up an aspect of the Tea Party that doesn’t fit the one party media narrative.

In the UK edition of Wired magazine is an article on the use of environmental markets in which, for instance, property developers or industrial users of water pay others, such as owners of wetlands or somesuch, if they want to make a development. The way the article is written gives the impression – at least in my eyes – of this being a great example of how capitalism and the Greens can work together. I am not so sure.

For instance, take the idea of “banks” of wetlands. Typically, what happens is that a government, such as the US one acting under legislation, will decree that there can be no net loss of wetland in given geographical area A, so if any area of wetland is destroyed, then the destroyers must offset this by paying to create another area of wetland somewhere. I immediately see a problem here: someone in authority has decreed that whatever happens to be the area of wetland at the time the new system is introduced is the area that must be maintained ad infinitum; but why not say that the area should be twice as big, or three times, or four times, or half as big? Also, the supposed “market” for such development permit trading depends on the existence of government regulations of certain areas, like wetlands, which might clearly go against the property rights of the folk who have owned those wetlands in the past and might have wanted to turn them into golf courses or whatever.

To be fair, though, the article does address the fact that property rights or markets of some sort represent a smarter way of addressing issues such as conservation, pollution and so on than traditional “lets just ban it” approaches used in the past. The article contains a great example of how the French mineral water industry did a deal with farmers over the latters’ use of fertilizer and pesticides in order to protect the water and keep the farmers happy. That is the kind of market transaction that works, and probably could have worked without government getting involved. My worry, though, is that a lot of such artificial markets in things such as environmental resources can become prey to corruption and mission creep of all kinds. Nigel Lawson, for instance, wrote dammingly about carbon trading in his recent book on the global warming controversy.

I would love to hear from AEP, or from Prof Congdon, exactly how creating money is supposed to create wealth.

If the Central Banks of the world buy private sector bank debt, they create new demand-deposit money that the private sector banking system can then lend. So more money units chase the same goods and services? Where is the new wealth?

– Toby Baxendale

With apologies to all for whom this is stale news, I want to report on Ezra Levant’s latest book. Remember Ezra Levant? Yes, the guy who put his head way above the parapet to defend freedom of speech against the ridiculous ‘Alberta Human Rights Commission’, which had been busy trying to stamp it out.

I have not been paying much attention to Ezra Levant lately, but last night I happened to re-visit his blog, and I soon struck gold. Or rather: black gold. Oil. Shale oil, to be more precise.

A commenter on this later posting by me here about Levant mentioned Canadian shale oil, and now Levant has written a whole book about this.

Canadian shale oil is taking a huge bite out of the market share of those Middle Eastern terror paymasters who have been such pestilential opponents of free speech in the West in general and of Ezra Levant’s free speech in particular, which could just be how Levant got interested. The Greenies hate Canadian shale oil, probably for that same reason. The Mainstream Media … well, that bit’s obvious. What’s not to love about a book saying hurrah for Canadian shale oil?

As I say, lots of Samizdata readers will have seen these bits of video, of Levant talking about this book, Ethical Oil (brilliant title, yes?), at least a week ago. I’ve only had time to watch and hear half of the first bit of video, but already I know that any Samizdata readers who do not yet know about this book will likely be very glad to hear about it now.

Many bad things have happened during the last decade. One of the best things to have happened during that same time is that books like this one of Ezra Levant’s – thanks to all of, you know, this – can now become as widely read as they deserve to be.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|