We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

When I heard Gordon Kerr speak in the House of Commons a week ago, I wished that he had done so with a microphone attached. Very early this morning he spoke in public again and this time he did have a microphone attached, because he was on Bloomberg Television. Turn up the volume on your computer and you’ll find it a lot easier to hear what he said this morning than I did last week.

Kerr confirmed my definite impression that the Austrianist team is now starting to win this argument. (By “this argument”, I mean, approximately speaking, this argument.)

Whereas regular academic economists talked about how this banking crisis was all over bar the recovery in 2008, the Austrianists have consistently predicted further disasters. As these disasters have duly occurred, the books and writers and ideas that the Austrianists keep referring to in their increasingly frequent public performances (Kerr mentions Hayek in this performance) are now breaking out of their academic-stroke-hobbyist ghetto and reaching the mainstream.

My favourite moment in this quiet little early morning Bloomberg TV conversation was when the man whom Kerr was arguing with said: “But if banks told the truth about the value of their assets, that would cause chaos.” His argument being that therefore making the banks tell the truth is a disastrous policy. Which it sort of is. But Kerr’s point, the point made by all Austrianists, is that disaster can’t now be avoided. The decisions that have made disaster inevitable have all now been made. By postponing the recognition of disaster, you only make it all the greater when it finally erupts.

Intellectual self-confidence is hugely important in a battle of ideas, such as we are witnessing now. The Keynesians, anti-capitalists, the more-of-the-samists, the borrowers-and-spenders and the rest of them, all want to believe that capitalism has to be managed by them if it is to work properly, in approximately the manner in which these people manage it now and have been managing it for the last few decades. Some of them still want to believe that capitalism itself ought to be smashed up, and entirely replaced by a planned economy. But how many people really think that this kind of thing would actually make the world more prosperous? The point is: the hatred of truly liberated, untramelled, uncontrolled, un-managed capitalism is all still there. But, the conviction that there is a superior statist alternative, not strong before this crisis became evident but briefly puffed up by the early stages of the crisis, is now fading away in front of our eyes.

Passionate and sincere belief in a viable, partly or wholly statist alternative to capitalism used to exist, in the early part of the twentieth century. Then, Marxists really believed that capitalism was colossally wasteful and inefficient, as well as colossally cruel and unjust and unfair, and that replacing it with a world run by small clumps of smart people with dictatorial powers, based in small but dictatorially powerful offices, would genuinely be a colossal improvement. They really and truly thought this. They believed it with the same certainty that naval tacticians, then and since, have believed (rightly) that vulnerable merchant ships are safer, during a merchant shipping war, if they all sail together in a convoy, rather than if every merchant ship sails alone. That being one of the arguments they used. This colossal Marxist and statist intellectual self-confidence was contagious and, when crisis hit Russia during World War 1 and the West at the end of the 1920s, it was hard to resist.

Now it is the Austrianists and only the Austrianists who have any genuine confidence in the correctness of their own ideas. Tiny in number but growing in number by the day, we Austrianists (I count myself a very junior member of this team – a fan rather than any sort of player) truly believe that we are right about how the world works, and about how it could eventually be made to work a lot better. This is why we are winning.

By winning, I don’t just mean convincing of our rightness third parties with no stake in how things are being done now and no power to make any difference, although that also will happen, in the fullness of time. I mean making our now hugely powerful opponents (powerful in the sense of having the power to go on doing huge damage) realise that they themselves are entirely wrong, and that we Austrianists, who until recently they had never even heard of, are right. I mean especially them. The bewildered onlooker tendency, vastly more numerous than any of the intellectual teams directly involved in this debate, is likely to remain confused about all this for a much longer time. They’ll only hear about this argument after we have won it. But the powerful people who presided over this long catastrophe, and who made and continue to make it ever worse with their ever more panic-stricken decisions, are mostly going to emerge from the wreckage with no doubt in their minds that their Austrianist critics understood everything far better than they did. They may not admit it out loud, still less formally surrender, although there will probably be some very public changes of mind. But most of these people will know in the privacy of their own minds that they were utterly defeated, by events, and by those who proved with their prophecies, observations and post mortems, that they understood these events, as they did not begin to until it was far too late.

It was like this with that earlier collapse of statist power, the fall of the USSR. The people who presided over that collapse had no doubt concerning the inferiority of their own economic arrangements, which was a big part of why those arrangements collapsed. It wasn’t merely that Soviet communism collapsed because it was hopeless. It collapsed because the Soviet communists who ran Soviet communism themselves came to realise that Soviet communism was hopeless.

Perhaps this is why Gordon Kerr talks so quietly. He is right. He knows he is right. He feels no need to shout.

Allow me also to remind you about Jamie Whyte‘s recent radio performance. He also spoke with utter certainty in the rightness of what he was saying, and he never once felt the need to raise his voice either.

LATER: Steve Baker MP comments.

Immigrants are incoming assets … in a global economy, their labour is vital both to tackle severe skills shortages and to fill long-term vacancies. Immigrants are not taking jobs that British workers could fill, but jobs which British workers are unable or unwilling to do … the idea that immigration is an intolerable burden on the taxpayer and the welfare state is baloney. Immigrants give far more than they take. It is estimated that they make a net contribution to the economy of £2.5bn …

– House of Commons Speaker John Bercow in an article in the Independent in 2005, quoted by Henry Oliver today in Adam Smith Institute’s Pin Factory Blog.

Since Detlev Schlichter is discussed frequently around here, I thought it might be interesting to write a summary of some of the arguments from his book, Paper Money Collapse. Of course I am summarising my understanding of the arguments, so caveats about my fallibility apply; errors and omissions are mine.

He begins with a description of money. It is the medium of exchange. It needs to be something people agree on. Ideally there will be a fixed supply which is infinitely divisible. Precious metals fit the bill. Schlichter distinguishes between exchange value and use value. It is possible to use gold for jewelery and electronic components, so it has use value. But as soon as it is used as the medium of exchange it is the exchange value that dominates. Money has value because it can be exchanged for goods and services.

When people say they want more money, what they usually mean is that they want more goods and services. Nevertheless there is a demand for money as a store of readiness to exchange, in preparation for near-future purchases or unexpected needs. Within the limits of his means, a person can hold exactly the money he wants at any time. If he wants more money, he stops buying stuff and perhaps starts selling it. If he wants less money, he buys goods and services.

If demand for money falls, then more people want to buy goods and services, so prices go up and the purchasing power of a unit of money goes down. This continues until the reduced purchasing power of money causes people to want more money. If the demand for money increases, then more people want to sell goods and services, so prices go down and the purchasing power of a unit of money goes up. This continues until the demand for money is met. In this way, the purchasing power of money changes almost instantly, so the demand for money is met almost instantly. There is no need to create money to meet the demand for money.

Does this cause prices to be volatile? Perhaps, but Schlichter argues that it is impossible for a central authority to control the supply of money quickly enough to counter changes in demand for it. The only way they can measure these changes is by observing prices. By the time the price has changed so that it can be observed, it is too late. He also points to empirical evidence that suggests that prices are more volatile when central banks control the supply of money. → Continue reading: Summarising Schlichter

A few minutes back I was glancing through Chinese trade statistics, in an attempt to put together the hopefully reasonably detailed post on what is going on in China that Brian has been nagging me to write.

With respect to Europe, the stat that pops out is that Germany runs a significant trade surplus with China, but that the eurozone as a whole and even more the EU as a whole runs a large deficit. Trade patterns with China are responsible for part of the immense stresses that now exist on the €uro. The German surplus puts upward pressure on the currency at the same time that the southern deficits put strong downwards pressure on it.

One thing that comes up is the “Hong Kong Problem” in the statistics. Many containers of Chinese exports from the factories of Shenzhen and Dongguan are carried over the border into Hong Kong, and are then shipped from the port of Hong Kong. Others are carried to the port of Shenzhen and then exported from China directly. Which port is chosen determines whether the export shows up in China’s trade surplus with America or whether it shows up in Hong Kong’s trade surplus with America. It is not difficult to simply consolidate the numbers, but this is not always done, and figures are sometimes misleading because of this. The two ports of Hong Kong and Shenzhen are only a few miles away from each other, and are at present third and fourth in the list of busiest container ports in the world, but would be the busiest by far if counted together. I had seen the port of Hong Kong many times prior to my last visit to the area in 2008, but I was curious about the port of Shenzhen, so I visited the Yantian district of Shenzhen.

After I wandered down the roads between warehouses and goods yards full of containers for a time, and took many photographs through gates, a man in a uniform gestured to me to stop and went of to consult with someone else in a more impressive uniform. At this point I thought it would be good to make myself scarce, so I departed rapidly down the road and out of the container port. (I sent a text message to a private equity fund manager friend of mine in South Africa, who urged me to keep taking photographs, as he was interested in seeing them, and because “Mike, your safety is something I am entirely willing to risk”).

But anyway, I made myself scarce. A half hour later I found myself walking along the shore past a rusting Russian aircraft carrier, which was apparently the centrepiece of a bankrupt, cold war themed theme park named “Minsk World”. After a while of this, I departed for a different area of Shenzhen, and somehow managed to end the day drinking a weissbier served to me by a young Chinese woman wearing a dirndl, while sitting on the deck of a boat that had once been Charles de Gaulle’s private yacht.

However, it was a good day. It is only on very special occasions that life gets this weird.

When buying two old Soviet aircraft carriers from the Ukrainians, the Chinese claimed that their reason for doing this was to convert them into tourist attractions. Reputedly, the actual situation was that they hoped to learn as much about aircraft carriers from them as possible, and then refit them as actual aircraft carriers. Upon discovering that they were in fact large and immense floating pieces of rust that had actually not been very good aircraft carriers in the first place, in a possible attempt to save face, the Chinese did attempt to convert them into tourist attractions after all. Thus the two Soviet military theme parks, one in Shenzhen based around the Minsk and the other in Tianjin based around the Kiev.

Both subsequently went bankrupt, a day out while looking at rusting remnants of the Soviet Union not apparently being a big attraction for the young Chinese. The Kiev carrier in Tianjin has apparently been subsequently converted into a hotel. The Minsk in Shenzhen continues to rust.). The Chinese in 1998 purchased the incomplete Admiral Kuznetsov class carrier the Varyag, which was at that point floating somewhere in the Ukrainian waters of the Black Sea. The carrier was officially bought by a Macau based tourist venture, with the pretext being that it would be converted into a casino. In this case, though, it remains in the hands of the Chinese military. After a (very) lengthy refit, it may one day enter into service in the Chinese navy.

All evidence is that the Chinese did in fact purchase Charles de Gaulle’s yacht with the intention of turning it into a floating Bavarian beer bar, however.

The pessimism expressed here for some time about China is now being expressed more widely.

Yesterday, via one of my favourite blogs, that of Mick Hartley (I especially like Hartley’s own photos), I found my way to some other photos by David Gray, of China and its newly minted ruins of the last decade and more. My favourite of these is the very first in the set displayed at the end of that link, which has what it takes to become “the” Chinese picture for right now.

It looks very impressive from a distance …

… but if you look at it closer up, it turns out to be a structure constructed by an idiot, full of steel and concrete, accomplishing nothing.

A few weeks ago, Samizdata’s travel and much else besides correspondent Michael Jennings, who has (of course) recently been in China (he has recently been everywhere), was talking of doing a piece about the mad building spree now, still, going on in China. I’d still love to read such a piece, but I fear that Michael may have missed that particular boat, in terms of revealing anything very shocking.

Happily, he did comment at length on an earlier short Samizdata posting about the Chinese construction bubble.

“All corporate taxes fall on households in the end. Companies might be convenient places to get cash from but they are not the people actually carrying the economic burden. It is some combination of shareholders, workers and consumers that are carrying the burden: those getting the social services which they are unable to fund.”

– Tim Worstall, dealing with yet another piece of nonsense from that over-blown socialist buffoon, Richard Murphy. I have to admire Tim’s stamina in how he relentlessly mocks and refutes the rubbish from Murphy. But someone has to do it.

This afternoon I visited the office of The Real Asset Co, and talked with Ralph Hazell (CEO), William Bancroft (Head of operations), and Jan Skoyles (Economist). I have hardly begun to digest the lessons I learned from what they told me. But in the meantime, let me at least supply a link to this video interview that Jan Skoyles did with Steve Baker MP, our favourite politician by some distance here at Samizdata. Jan Skoyles is living proof that you can earn a living as an “economist” without knowing an enormous pile of things which are not so.

More and more, I find myself fearing that Baker is just too good to be true, and that some frightful skeleton will one day soon come tumbling out of his closet. I have absolutely no rational basis for such fears. It is just that the man is a politician.

I recall sitting next to Baker at a Cobden Centre dinner about a year ago, and rather rudely telling him that I expect from him: absolutely nothing, on account of him being a politician. He has already far surpassed my wildest fantasies. This video interview once again had me blinking in disbelief at the sheer uncompromising sensibleness of what he was saying. I did take a nap earlier this evening. Was I dreaming again? Apparently not.

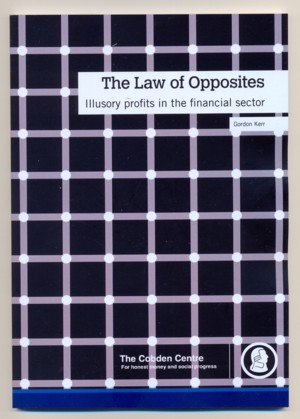

This afternoon I attended an event in the House of Commons organised by the Adam Smith Institute, to launch their publication (published in partnership with the Cobden Centre) entitled The Law of Opposites: Illusory profits in the financial sector, by Gordon Kerr. Kerr himself spoke.

Alas, Gordon Kerr is a rather quiet speaker, and he did not use a microphone. Worse, after the talk had begun, I realised that right there next to me was some kind of air conditioning machine whirring away, in a way that made following Kerr’s talk difficult. Live and learn.

But I got the rough idea. Bad accountancy rules make disastrously unprofitable banks seem like triumphantly profitable banks, and those presiding over these banks are paid accordingly, even as their banks crash around them. And much more. The ASI’s Blog Editor offers further detail.

Good news though. I, like everyone else present, was given a free copy of The Law of Opposites. See if you can spot why I am reproducing the cover here. I am sure this will not take you long. I was interested to see if the effect in question would survive my rather primitive scanning skills. It does:

This publication is quite short, less than a hundred pages in length. Even better news. You don’t have to buy a paper copy like the one I now possess if you don’t want to. You can read the whole thing on line.

I am on the Cobden Centre email list, and I have to be careful about confidentiality with regard to many of the emails I read. However, the one I just got today from Jamie Whyte is presumably intended to get around:

I’m on BBC’s Radio 4’s PM programme tonight, discussing the report on the FSA’s failure to notice that RBS was about to fail – up against some former official of the FSA. I am afraid they are going to edit what I said (fingers crossed on that) and also that I cannot tell you the exact time my item will come on the programme, which starts at 5pm, I think.

The FSA is the British financial regulator. RBS is the Royal Bank of Scotland. According to the man from the FSA, the Royal Bank of Scotland’s woes were caused by poor decisions.

I’m guessing that Jamie Whyte will be a bit more informative than that. I am out and about this evening, but it looks like there’ll be a recording available, for a while. If nothing else, this is further evidence that the Cobden Centre gang are putting themselves about.

LATER: I managed to listen to Jamie Whyte’s performance, and better, to record it. Here is what he said in his opening statement:

[The FSA] did fail. But I don’t blame it on the individuals of the FSA. I think that they have an impossible task. What’s happened in banking is that because of government guarantees to those people who lend money to banks, explicitly in the case of retail depositors – you and me with our ordinary money in the bank, and implicitly and pretty reliably in the case of wholesale lenders to banks, because they’re government guaranteed, there is no price mechanism any longer in the banking market for risk. So banks can take as much risk as they like and without paying a price for it. Normally what would happen in a free market is that it would become more expensive for banks to borrow money. And that doesn’t happen. There’s no risk premium for banks taking larger risks, because the people lending the money realise that the government will bail them out.

Now the effect of this is that basically the government is subsidising bank risk taking on a massive scale. And the job of the FSA is to counteract that. There are these rules – the Basel rules and so on about capital requirements. And then there are supervisors, regulators, people who go into the banks and check they’re complying, and their job is to counteract the massive incentive towards risk taking that the government has already provided. Now the question is: can they do it? They obviously failed to do it. Can they, if they do a better job? And I think they can’t.

And the reason they can’t is that there are almost infinitely many ways that banks can take risks. The rules will always specify some particular ways, and regulators will go in, looking at that stuff. Are they doing this or that? But the bankers are very clever and they can always come up with other ways of taking risks, and I just think it’s a hopeless task that they’ve been given.

Whyte’s opponent in the debate, a Mr Jackson, got off on the wrong foot at the start of his reply:

I think it’s very easy to blame the regulators.

Which many are indeed doing, but not Jamie Whyte. His point was that their task is impossible.

Mr Jackson went on to say that he thought that the regulators could do better, by, you know, doing better. And the BBC gave him the last word. Which was him saying that the regulators could indeed … do better.

But Jackson never really said why he thought this. There was talk of cats and mice, and of how the mice are very numerous and very incentivised and the cats unable to cope. The general idea was aired of making regulators less numerous, better paid and above all “better trained”, and of having these few regulatory titans apply only one simple all-embracing regulation, rather than lots of regulations (with lots of omissions), namely: Banks must behave well! Putting the regulators entirely in charge of banking, basically, although that was not quite spelt out. It was classic Road to Serfdom stroke Economic Calculation stuff, with one guy saying that calculation is screwed and should be unscrewed by the state retreating rather than advancing, and the other guy saying: we can still regulate better in the future (despite the evidence of the recent past), by making the arbitrary power of the state even more arbitrary and even more powerful (and hence even more likely to screw things up on an even grander scale in the future).

Just who “won” this argument is anybody’s bet. I think that Whyte made a much stronger case than his opponent, but I would, wouldn’t I?

More to the point, anyone generally inclined to favour free markets, capitalism, etc., to favour rational economic calculation and to oppose serfdom, would definitely have scored it a win for Whyte on points. Such a person might even want to dig further into the argument with some internet searching. At which point the fact that Whyte is spelt with a “y”, and that Whyte was introduced only as a “financial commentator” (rather than being from, say, the Cobden Centre) won’t have helped any.

Perhaps this posting will help such searchers after truth rather more.

I cannot claim to grasp much of the detail of all the drama now surrounding the EUro. This photo, taken by me yesterday, captures the feeling of it all quite well:

Click to get that bigger and more legible.

Is all this drama being cranked up to enable Cameron to take the credit from us Brits for bollocking up the Euro, and simultaneously to enable everyone else in EUrope to blame us? Just, as Americans say, askin’.

One little titbit of news that does strike me as particularly interesting is this, in the Wall Street Journal, about how various governments are quietly pondering EUro-alternatives. At the very least, someone at the Wall Street Journal is asking about alternatives.

It all makes me think of those bridges that Julius Caesar burned, so that his army then knew that they would either fight and win, or perish. Except that this time, various parts of the army are nipping back to the various rivers that they just might be wanting soon to be retreating across, and are quietly building bridges. Just as burning bridges changes the game, so does building them. Even thinking about building them changes things.

I greatly enjoyed this article by Kevin D. Williamson about Thomas Sowell. Sowell is now in his eighties. When somewhat younger, he looked like this:

Here is what is probably the key paragraph in Williamson’s Sowell piece:

Because he is black, his opinions about race are controversial. If he were white, they probably would be unpublishable. This is a rare case in which we are all beneficiaries of American racial hypocrisy. That he works in the special bubble of permissiveness extended by the liberal establishment to some conservatives who are black (in exchange for their being regarded as inauthentic, self-loathing, soulless race traitors) must be maddening to Sowell, even more so than it is for other notable black conservatives. It is plain that the core of his identity, his heart of hearts, is not that of a man who is black. It is that of a man who knows a whole lot more about things than you do and is intent on setting you straight, at length if necessary, if you’d only listen. Take a look at those glasses, that awkward grin, those sweater-vests, and consider his deep interest in Albert Einstein and other geniuses: Thomas Sowell is less an African American than a Nerd American.

My strong is Williamson’s italics.

I’d never thought of Sowell as being anything like this guy …

But yes, I guess maybe there is a resemblance. Here is link to a brief snatch of video of Moss saying something very Sowellish, about the importance of getting a good education.

By the way, I am not calling the actor and director Richard Ayoade a nerd. I don’t know about that. But I do know, as do all who enjoy The IT Crowd, that Ayoade’s TV creation, Moss, most definitely is a nerd, and a nerd first and a black man way down the list, just as Williamson says of Sowell.

Although, as a commenter said of this bit of video: “Richard has a bit of Moss in him.” A bit, yes. But what has really happened is, surely, that Ayoade was a nerdy kid, and has kept hold of it for comic purposes.

I suspect Sowell did something similar, and, as Williamson suggests in his article, in a more courageous and significant way. He too was a genuinely nerdy kid, who could understand truth better than he understood the demands of fashion. Then, when he got older and started to tune into the zeitgeist, he had to decide if he was going to shape up and get with the liberal (in the American sense) fashions of his time or stick with that truth stuff he had got to like so much. He stuck with the truth.

Also, I don’t believe Sowell would ever remove a water tank (see the second of the two video links above) and then be surprised that his plumbing no longer worked properly.

By the end, we may see profligate politicians hanging from lampposts. But there’ll be a lot of bad stuff, too.

– Instapundit

LATER:

But all joking aside, if the current profligacy continues, and America winds up in a Greece-style (or worse) collapse, politicians may not wind up hanging from lampposts (we don’t really do that here), but they will at the very least likely face the kind of investigations, prosecutions, and social opprobrium normally reserved for child molesters and Bernie Madoff types. I don’t think they fully appreciate that. If they did, they’d be acting differently.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|