We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

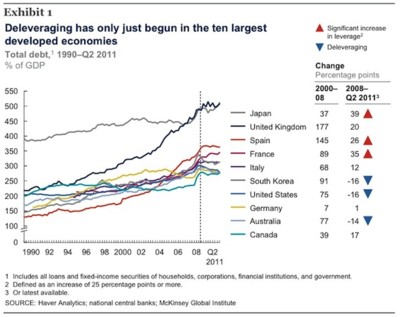

Tom Clougherty has an interesting graph up at the ASI blog, taken from this McKinsey report, of the movement in combined public and private debt for the ten biggest of the world’s developed national economies, from 1990 until now. Follow either of the above two links to get a bigger and more legible version of this graph:

Since 2007, of course, all have lurched upwards from wherever they were to quite a bit more.

To me the interesting bits are those between 1990 and 2007. The general trend was a general increase in debt, from somewhat troubling to somewhat more troubling. But three countries bucked this trend: Japan started very bad and merely stayed very bad; Canada started okay-ish and stayed okay-ish; Britain started okay-ish but became very bad. In terms of the direction things went in, Canada has the best graph of them all, and Britain has the worst. Between them, these three graphs, the grey one along the top (Japan), the green one in the pack towards the bottom (Canada), and the dark one moving most determinedly upwards (Britain), make a kind of big and elongated Z.

One other deviation from the norm worth noting is that just before 2007, Germany, unlike any other country, went (see the yellow graph) definitely downwards. It did what Keynes said, in other words, and paid down its debts when times were good, or at least when they seemed good. In Britain, the “Keynesians”, public and private, just carried on running up more debt.

I know that as a fan of Austrianism I am not supposed to get too excited about national economic aggregates. But this set of aggregates and aggregate movements looks to me quite telling. Make of it all what you will. For me, it confirms the sense that many now have that Tony Blair’s government was one of the worse ones that we’ve ever had.

This article over at the Foreign Policy website, by Helen Mees, dusts off an argument that I have mentioned here on Samizdata before, (in relation to a comment by the US investor and commentator Peter Schiff) namely, that China, by using its vast foreign exchange reserves to buy Western government debt, thereby pushed down long-term interest rates and encouraged the kind of reckless lending that ended up going ker-boom! in 2007-2008. And if only the Chinese had not flogged us all those artificially cheap computer parts and children’s toys (made cheap by that naughty fixed exchange rate regime for the yuan), they would not have made so much money to then lend to us Westerners to blow on housing we cannot really afford. (Here is another old post of mine on the same subject of debt/savings imbalances between the West and China.)

The problem with this line of reasoning is that if, say, a country has earned genuine income by selling something valuable and useful (like toys, cars, electronic components or whatnot), and invested the proceeds abroad in things that can generate new wealth in the future, what is the problem? The problem is not that China invested huge savings and other surpluses into the West – after all, in the 19th Century, the UK invested large capital surpluses in places such as the US, Canada and Argentina (now there’s an irony, Ed). And there was nothing “imbalanced” about that. If real savings – not central bank funny money created out of thin air – gets lent to people to invest, that’s hardly bad. The problem is if the money is lent to people buying homes as part of a broader speculative bubble in real estate, say. And there is no doubt that domestic policy in the West, most definitely in the US, encouraged unwise lending and borrowing for property, consumer goods and so on, rather than investment in new technologies and industries.

The comment thread on the FP item are interesting, where it is contested that subprime borrowing made up only a tiny fraction of the US mortgage market. It did not, since one of the issues with the sub-prime market and the huge losses sustained by banks was how sub-prime debt was mixed up with better quality stuff and then sold to investors as if it is was all investment-grade, when it was wasn’t. For example, here is a comment from a person called “RRAFAY”:

“Actually, 5% of Subprime is enough to cause a crash. Especially, when no mention is made of how these mortgages were leveraged. Secondly, Alt-A is not mentioned either. When both are taken together, they represent roughly 15% of the US mortgage market. Secondly, the idea that Chinese surplus capital led to an excess supply of money is so weak, that it is mind boggling that someone would even suggest this. China only holds 7% of total US debt. Each country mentioned had a housing crisis, Ireland, Spain, and the US.”

In my view, it is certainly true that in a world of free capital movements, if a country A can export a vast amount of its capital into country B, and people in the latter country are not constrained by proper market disciplines and there is already a full-blown encouragement of high borrowing and lax lending, then the added money will pour fuel on the fire. But in the main, I think it is a pretty silly line of argument to say that it is the fault of the Chinese for having earned so much money and then reinvested it. There’s something just not quite right about that argument on so many levels.

Comment just attached, by “Malcolm”, to my posting here a while back entitled Austrianism as Number Two:

Newsnight has just introduced its story on Ed Milliband’s decision today to back the government’s pay freeze by playing the Keynes v Hayek video from Econstories.tv

The narrator even described it as a “fabulous” video that is “easily the most entertaining explanation of the issues” – as closely as I can remember the wording, anyway.

I realise I’m commenting on a posting that’s six months old, but I’m hoping Brian, as the original author, gets automatically notified of comments. That the video is being used to give context to a now-current news item is certainly consonant with Brian’s original theory about Austrianism as the new #2 (with apologies to The Prisoner).

I did get automatically notified of this comment. Many thanks for the kind thought. However, I also clocked this Newsnight snippet myself, and added an off topic bit in a comment I also added to the earlier posting today about SOPA, which Newsnight is also reporting on, thanks to the Wikipedia black-out that Rob Fisher noted.

The more I ponder those Keynes v Hayek videos, the more of a stroke of total genius I believe them to be. They play especially well with the BBC, because the BBC is never happier than when explaining an issue in terms of competing arguments. Yes, the BBC is often “biased”, in the sense that you get a definite idea of which team they may prefer (which may not be yours), and which team they choose to give the last word to. But the “other” team often gets a more than fair crack of the whip.

As I made clear in that earlier posting of mine, the real sufferers from this kind of bias are the “other other” teams, so to speak, the ones who don’t even get a look in, the ones who are shown as being not even wrong, on account of not even existing.

To quote Rob Fisher in the posting immediately below, about Detlev Schlichter’s performance on the BBC’s “Start The Week” show yesterday morning:

All in all not a bad day for the spreading of Austrian ideas.

Which adds up to two consecutive not bad days for the spreading of Austrian ideas.

As Brian Micklethwait informed us ahead of time, Detlev Schlichter appeared on the BBC Radio 4 programme Start The Week on Monday. A podcast of the programme can be downloaded. Remember that all of this is being talked about on the BBC, on Radio 4, which I imagine is listened to by lots of Guardian and Independent readers. Austrian economics is now Being Talked About, as Brian might point out.

The programme opens with Economist columnist Philip Coggan talking about the supposed conflict between money as a store of value and money as a medium of exchange. Creditors will always want a fixed supply of money and debtors will want an expanding supply of money, and this seems true enough, up to a point. Coggan goes on to point out that the biggest debtor is government and governments have always been very keen on expanding the money supply. He also explains how banks’ interests are aligned with the governments because the expanding money supply props up asset prices. There is no way out except by defaulting or inflation.

Angela Knight of the British Bankers Association is worried about more immediate matters like tomorrow and the Eurozone crisis.

Detlev Schlichter is up next. He says that paper money systems have been tried throughout history and have always failed; have always been implemented to fund the state. The failure mode is either a return to commodity money or hyperinflation. He clarifies Coggan’s point about conflict between debtors and creditors by pointing out that in a voluntary contract both expect to benefit. They would both like a means to honour that contract with money that they can trust. This makes sense because if debtors routinely get the expanding money supply they want, this ultimately will get factored into the price of the loan.

Coggan says that the trouble with the gold standard is that it imposes more austerity on governments than the voters will stand. I think Schlichter agrees, which is why he is predicting hyperinflation.

Maurice Glasman says that capitalism requires ‘exploitation’ of humans and their environment and short term returns. Detlev is ignoring the imbalance of power between the debtor and creditor. After that I couldn’t follow what he was on about.

Schlichter responds to Marr’s questions by saying that expanding money supply is right now being done to stimulate the economy rather than just to fund governments. Furthermore he is not suggesting that we walk around with little sacks of gold; payment technologies do not depend on state fiat currency. The BBC listeners are reminded that money is not backed by gold and that it’s just an invention of the state. Schlichter advocates removing the state entirely from money. Consumers should control what is produced in the economy by sending price signals, but this does not work because of the expanding money supply. If we went back to gold, as has been done before in Britain, markets would correct. Andrew Marr is incredulous: interest rates shooting up!? In this day and age? Yes, says Schlichter, calmly, it is essential that savings and investments are coordinated by interest rates.

Philip Coggan says going back to gold is possible but very unlikely, but could arise from complete collapse of the system, Zimbabwe-style, but this is not imminent in the next two or three years. Schlichter agrees that politicians are unlikely to take that decision. Over the last 40 years, since the whole world has been on paper money, we have had unprecedented money expansion and, surprise surprise, the whole world is in a mess. If we suddenly went back to hard money now it would cause a sharp correction and a recession. So Politicians will avoid this and in so doing cause a worse outcome.

Angela Knight is asked whether bankers are failing savers by getting into league with the government and she avoids the question, but agrees that banks should not be protected and should be allowed to fail. But there are a lot of Buts that I didn’t follow.

Philip Coggan says bankers have become so important because of the credit money expansion of the last 40 years. For some reason he brings international trade into the conversation. Knight starts waffling about ATM machines and the disruption to people’s lives that a move to gold would entail. Schlichter says that gold works fine in an international economy (after all, gold is gold wherever you are). When he talks about disruption he is talking about the correction of the accumulated imbalances in the economy. It’s clear he doesn’t know what Knight is on about, either.

Maurice Glasman makes a distinction between… oh I give up. The man is completely incomprehensible.

Coggan and Knight dignify him far too much by conversing on his terms, which wastes most of the last 15 minutes of the programme. Schlichter disagrees with him completely and gets in a point about how Germany’s success after WWII is a result of its relatively hard currency which encourages savings and avoids asset bubbles.

So there we have it. Coggan and Schlichter have their differences but would have appeared very close to each other to the BBC listeners. Knight didn’t really say anything, and Glasman was the token lefty who only other committed lefties would have been cheering along with. All in all not a bad day for the spreading of Austrian ideas.

“Certainly there is a need for free-market economics to be rescued from those who distort and discredit it, but that is the argument that must be made: that this system has delivered mass prosperity (and the self-determination that comes with it) on a scale unprecedented in human history, and that it deserves to be saved from the spoilers.”

Janet Daley, writing with justified scorn about those people who have been bashing Mitt Romney for his career in venture capital at Bain. To be honest, his background in this area is one of the few things going for him. It would be quite refreshing to have a president of the United States who can actually read a balance sheet.

For those who have not come across the “creative destruction” line before and how it applies to sometimes wrenching change in business, check out the great Joseph Schumpeter.

As a caveat, I should add that some – but no means most – private equity buyouts of firms have been made possible by cheap credit, and therefore might not have occurred in the way they did had interest rates not been how they were in the past decade or so. On a related point, here is what I wrote in defence of private equity at Samizdata several years ago. Excerpt:

“In the main, what these firms do is target cash-rich firms that are run by often lazy executives who have presided over crappy business decisions. Take the meltdown of Marconi a few years ago, one of Britain’s most famous companies. That was a listed company. The destruction of value and jobs in that company remains, in my mind, one of the most disgraceful episodes in British corporate history and who knows, it might have been saved from making big errors had a private equity fund been in charge, rather than deluded executives. Private equity firms helped stymie Deutsche Börse’s foolish bid for the London Stock Exchange 2 years ago, and have turned around businesses. They typically buy and hold a firm for 5 years or more, take a hands-on approach to running firms before spinning them off to another buyer or floating them in an IPO. So Will Hutton should spare us sentimental guff about how limited liability firms floated on the stock exchange represent the perfect model of doing business or something that Adam Smith or Voltaire would exalt. They are merely one of the many ways in which economic activity manifests itself. As interest rates rise and the economic cycle turns, some of the excesses of leveraged buyouts will fade and private equity transactions will decline.”

Austrian economic theory describes how purposive action by fallible human beings unintentionally generates a grand, complex, and orderly market process. An additional ethical step is required to pronounce the market process good. Economic theory per se cannot recommend but only explain markets. This is what Ludwig von Mises meant when he insisted that Austrian economics is value-free. Anyone of any persuasion ought to be able to acknowledge that economic logic indicates that imposing a price ceiling on milk will, other things equal, create a shortage of milk. But that in itself is not an argument against the policy. Mises assumed the policymaker would have thought that result bad, but the economist qua economist cannot declare it such. As Israel Kirzner likes to say, the economist’s job in the policy realm is merely to point out that you cannot catch a northbound train from the southbound platform.

– Sheldon Richman writes about How Liberals Distort Austrian Economics

Incoming from Detlev Schlichter:

Just a heads-up in case you are interested, I will be one of four guests on Andrew Marr’s show Start the Week on BBC Radio Four on Monday, 16th January. The program starts at 9 am but there are various ‘listen again’ facilities, and it will also be published as a podcast. The topic is the financial crisis, and the other guests are The Economist’s Philip Coggan (author recently of Paper Promises), Angela Knight, chief executive of the British Bankers’ Association, and the Labour life peer Maurice Glasman.

I am interested.

If we immerse ourselves wholly in day-to-day affairs, we cease making fundamental distinctions, or asking the really basic questions. Soon, basic issues are forgotten, and aimless drift is substituted for firm adherence to principle. Often we need to gain perspective, to stand aside from our everyday affairs in order to understand them more fully. This is particularly true in our economy, where interrelations are so intricate that we must isolate a few important factors, analyze them, and then trace their operations in the complex world.

– from the Introduction of What Has Government Done To Our Money? by Murray Rothbard. To read the whole thing, go here.

I link a lot to the sayings and doings of Steve Baker MP (that being the last time I mentioned him here), so this time I will be brief, and only say that I like the phrase “new money being loaned into existence”. The piece this phrase appears in is entitled Could this be a second crisis of state socialism? If you are already saying to yourself something along the lines of: “yes I rather think it could be”, you will, you will be unamazed to learn, find yourself in agreement with Mr Baker.

“American economist Scott Sumner has recently argued that the Fed cannot be blamed for the inflation that led to the Wall Street Crash because the money supply measures that reveal the inflation were not publicly available at the time. As Robert Murphy has responded, the fact that doctors of the time didn’t understand bacteria does not affect the cause of deaths during the bubonic plague. Whether we “blame” central bankers or not is really a secondary consideration to our attempts to understand what happened and why. By assigning blame we suggest that the Fed should have done better. It encourages us to think “if only it did X everything would be ok”. But the problem isn’t that individuals focused on the wrong targets, and the solution isn’t to work out how they can improve. The lesson should be that the nature of central banking – the attempt to centrally plan the monetary system – imposes an epistemic burden on policymakers that they cannot possibly ever fulfil. The Fed wasn’t to blame for the crisis, because any argument for what it “should” have done is insincere. We should absolve it from culpability, and remove the shackles of expectation that we place upon it. It did the best it could be expected to do. And that wasn’t enough.”

– Antony J Evans, economist and what I would call a “sensible-shoes Austrian”.

“One of the more unexpected things I discovered as CEO of a pharmaceutical company was that I had to think as much or more about the federal government than I did about our competition. I had known on an intellectual level that government was involved in the private sector in a great many ways, but it was only when I was actually in business that I felt the full impact.”

Donald Rumsfeld, Known and Unknown, page 253. He is describing his time in the private sector during the late 70s and 80s, and emerges as quite a firebrand for supply-side economics (he got to know Arthur Laffer).

Whatever you think of Rummy as a defense secretary (under the Ford and George W. Bush administrations), he comes across as a formidable man of US public and commercial life.

Here is something that I wrote about the FDA and associated drug regulation issues a while ago here.

“Open-source intelligence has always been crucial, but for most of the cold war it was neglected by western intelligence agencies,” says Calder Walton, a research associate at Cambridge University and author of the book Empire of Secrets, to be published in 2013. “That was the archetypal intelligence war: intelligence necessarily involved information that couldn’t be gained from any other source — human agents or telephone tapping.” That doesn’t mean covert intelligence was more effective, though: Daniel Moynihan, a former US senator, compared CIA reports gathered from secret sources with Soviet documents recovered after the fall of the Berlin Wall and found they significantly overestimated Soviet capabilities. But he discovered that western think tanks using publicly available material, such as the RAND Corporation, were much more accurate. US diplomat George Kennan estimated in 1997 that “95 per cent of what we need to know about foreign countries could very well be obtained by the careful and competent study of perfectly legitimate sources of information open and available to us”.

Excerpt from an article in Wired, the tech and futurism magazine, about a Swedish investment firm, Recorded Future, that is taking the use of social networks and other systems to new heights in its attempt to get a jump on the market. In the process, it sheds new light on how the intelligence-gathering process works.

Here’s another couple of paragraphs:

The 20 employees of Recorded Future aren’t foreign-policy experts. They aren’t traders either, but if you’d started using Recorded Future’s predictions to buy US stocks on January 1, 2009, you would have made an annual return of 56.69 per cent. (The S&P 500 had an annualised return of 17.22 per cent over the same period.) Between May 13 and August 5 this year, as markets behaved with vertiginous abandon, their strategy returned 10.4 per cent; in contrast, the S&P 500 lost 9.9 per cent of its value. They’re data experts: computer scientists, statisticians and experts in linguistics. And in the data, they think, lies the future.

All Recorded Future’s predictions, whatever the field, are based on publicly available information — news articles, government sites, financial reports, tweets — fed into the company’s own algorithms. The result, it claims, is a “new tool that allows you to visualise the future” — one that is changing how government intelligence agencies gather information and how giant hedge funds place bets. On its website, Recorded Future states: “We don’t grant interviews and we don’t issue press releases.” But behind closed doors, the company is developing the technology that has been described be one tech blog as an “information weapon”.

The businesses was founded by a chap called Christopher Ahlberg, a former member of Sweden’s special forces and a serious entrepreneur. In its own way, this article is just another example of how Sweden is not quite the socialist nation that it is sometimes said to be, either by its starry-eyed admirers or detractors. There is a lot of entrepreneurial zest up there in the frozen north, it seems.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|