We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

“If it [naked short selling] lowers share prices, that is because companies were overvalued. If the companies get into trouble as a consequence, that is because they were bad companies, not good ones. Bad companies deserve to be punished for being bad companies, so that capital can be better allocated elsewhere. (And yes, I am talking about the benefits of making it easy to take short positions *in general* rather than talking about the naked/covered distinction, which is a technical issue that I don’t actually think matters much. It may actually be better to discourage this and instead encourage people to take short positions via derivatives markets, which they can easily do). The truth is that we have had massive capital misallocation in recent decades. Capital has been far too cheap, and much investment has gone to all kinds of stupid places where it cannot generate a genuine economic return. Many companies have believed that they were good companies when in fact all they were doing was milking the fact that they had an unrealistically cheap cost of capital. For the last five years or so, this state of affairs has been ending, which is horribly painful. It would be over quickly if more people (politician, homeowners, and stakeholders in companies doing useless thing) would actually get it into their stupid heads that it has to end.”

Our own Michael Jennings, whose comment on my post of yesterday was too good to leave in the associated thread. I suspect this DVD, The Wall Street Conspiracy, will soon be heading for the trash can. I am wary of any “documentary” that starts from the premise that people in financial markets are like Bond villains destroying profitable firms in ways that make no sense even for the supposed “villains” in the case. For me, the key issue is transparency: if you are shorting a stock in a firm or whatever, and your counterparty is fully consenting to the transaction and you both understand the risks and don’t expect to get bailed out, then such activity should be put in the same category, IMHO, as off-piste skiing – risky but not criminal and certainly not fraudulent.

A while back, in a posting here about a meeting at the House of Commons addressed by Detlev Schlichter, at which James Delingpole was also present, I speculated that maybe Delingpole might at some point in the future choose to get stuck into the question of what has been going wrong with the world’s financial system.

So, I was delighted to encounter this recent Delingpole posting, about why the price of oil is going up. He features a video of Ron Paul saying that if you print lots and lots of money, everything goes up. Or, to put it another way, it’s not oil that is going up; it’s fiat money that is going down.

I see that Delingpole gives the Cobden Centre an appreciative mention, which will please them greatly.

Delingole, whose idea-spreading abilities I admire more and more, is a significant voice in the world. He has a huge following, which is well deserved. He takes important ideas seriously, but himself not so much, in a most engaging and yet informative way, the proof of his effectiveness being how much he gets up the noses of whatever bad guys he takes aim at.

If Delingpole could do to the world’s central banking racket what he has already done and continues to do to the world’s “climate science” racket, that might really be something.

“Yelling “fire” in a crowded theater is a terrible thing to do — unless there’s a fire.”

Thomas Dolan, Barron’s. He was writing about a wonderful financial market practice – sometimes legal, sometimes not – known as “naked short-selling”. His article explains what that means. I got interested after getting a DVD in the mail, called The Wall Street Conspiracy, that reckons that this practice was responsible for destroying many an honest business. Sounds a bit like Michael Moore, but I will give it a view to see if it stacks up or is a pile of crap. One quick thought: the idea of selling something you don’t own or haven’t even borrowed yet does sound awfully close to outright fraud, like insuring a house against fire if you don’t even own the house. Or like fractional reserve banking……….Aaarrgggghhh…

Bishop Hill and WUWT are both making much of this:

To be effective, a new set of institutions would have to be imbued with heavy-handed, transnational enforcement powers.

If CAGW-inspired regulation is to make any sense, it must be universal. There must be a World Government. There are those of us who have long believed that this was why CAGW was devised in the first place.

Time was when economic success was believed to result from such “cooperation”, and to impossible without it. So, the language of tyranny was economics. Then – alas for the tyrants – it became clear that economic success and tyranny are opposites, although that lesson has still to be completely learned.

Now, the language of tyranny is a different kind of “science”.

Here is a list of things that you can buy, but which Michael Sandel (who I seem to recall doing a series of lectures for the BBC – yes) thinks it’s morally dubious for you to be able to buy.

I haven’t read all of them, but was immediately struck by this one, which strikes me as, on the face of it, a very good idea:

The right to shoot an endangered black rhino: $250,000. South Africa has begun letting some ranchers sell hunters the right to kill a limited number of rhinos, to give the ranchers an incentive to raise and protect the endangered species.

To Michael Sandel, this seems to mean that South Africa is being bad. But to me it sounds like South Africa is serious about preserving its now endangered black rhinos.

I have a definite recollection of noted South African libertarian Leon Louw having recommended just such a thing. I wouldn’t be at all surprised to learn that he was partly responsible for this arrangement.

I myself won’t comment in detail on the rest of Sandel’s piece. It is complicated and I am about to go to bed. Parts of what he says strike me as true, parts not. But me saying only that needn’t stop other commenters going into more detail.

Spring is in the air, and there is a spring in the step of the climate skeptic blogs these days, the two big ones on my radar being Bishop Hill and Watts Up With That. Peter Gleick‘s trickery, already written about here by Natalie Solent, combined with the willingness of so many on his team to try to promote him as some kind of hero rather than condemn him as the failed fraudster that he is (see also this posting about Michael Mann), means that although climate skepticism hasn’t won, it continues to win. Slowly but surely, C(atastrophic) A(thropogenic) G(lobal) W(arming) is being reduced from “science” to a racket.

Declarations of complete victory are surely premature. Much depends on how you define victory, and who or what you consider to be the enemy. If you care only about scientific truth, but not about the world being littered with damaging and expensive bureaucracies dedicated to perpetuating and enforcing lies, you may well indeed believe this battle to be nearly over. If those bureaucracies (to say nothing of the larger financial and ideological interests they serve) still trouble you, as they do me, you will regard the war as hardly having begun.

Some are saying that continuing to argue about the mere science of it all is a distraction from the more serious task of unmasking the motives and machinations of all those personages to whom all this fraudulent science has been so useful. I disagree. I say that showing this “science” to be dishonest leads naturally on to the question of who patronised it and to what end, given that the mere truth of things was emphatically not the only thing that concerns all those concerned. If the science of CAGW was now, still, universally accepted as honest, the underlying intentions of the various factions and characters responsible for foisting it upon the world would not now be attracting nearly so much scrutiny.

An immediate next task for the skeptic tendency is to itemise and publicise, in greater detail than hitherto, who is making money out of CAGW, a process that is already well under way. The longer term goal is to unmask the politics of it all. The bigger goal behind this hoax (and many others) was, and remains, to turn the entire world into a corrupt tax-and-spend superstate, run for the pleasure and enrichment of anti-progress, screw-the-poor-in-the-name-of-the-poor, global despots. That many very useful and desperately sincere – very useful because so desperately sincere – idiots are and always have been involved in this project is not in question. These idiots need to be challenged intellectually rather than merely denounced as crooks and tyrants, although showing them that crooks and tyrants is who they are really supplying aid and comfort to may also help to straighten them out.

In the post, and I should have read this book months ago: Watermelons. James Delingpole has been a key figure in ensuring that the CAGW ruckus (and the Climategate story in particular) escaped from the ghetto of blogs like the ones I linked to above, into the general arena of political discussion, and even to infect parts of the general public, now so curious to know why their heating bills are going ballistic. The thing about Delingpole is that not only has he done a fine job publicising the various scientific criticisms of the CAGW faith. He also understands what set the whole thing in motion in the first place. He gets the money of it. Above all, he gets the politics of it. When I have read this book, I’ll surely want to say more about it here.

Charlie Stross writes great science fiction and a blog which usually leaves me wondering how I can enjoy so much the novels of a man with whom I agree so little. In a recent post he linked to an article by UCSD associate professor of physics Tom Murphy to explain why space colonisation will not happen. Since the site is called “Do the Math” I was expecting some numerical analysis of space colonisation. Instead the article contains lots of reasons why space travel is hard and slow and requires lots of energy and is not likely to be done much more by NASA, but nothing that suggests it violates the laws of physics.

I like physicists. They do real science that gets answers from proper observations. So I was a bit disappointed by the space article and went in search of goodness. There must be some good insight that a physicist like Murphy can offer.

He analyses the growth of energy consumption. Since 1650, total energy usage of the United States has increased by about a factor of 10 every 100 years. If energy production continues to accelerate at this rate, we’ll heat the atmosphere to 100C in 450 years. Murphy is not saying this will happen, he is saying that there is a limit to how much energy we will want to produce. So far so good. But how much energy can a person use? Why does it matter?

Once we appreciate that physical growth must one day cease (or reverse), we can come to realize that all economic growth must similarly end. This last point may be hard to swallow, given our ability to innovate, improve efficiency, etc. But this topic will be put off for another post.

So this is to be a Limits To Growth argument. In this other post Murphy talks a lot about the limits to how energy efficient things can be. He is right that it will always take a certain amount of energy to heat food, for example, and that there are processes that can not be improved beyond physical limits. But he seems unable to imagine economic growth without growing use of energy. Doing the same task with half the energy, something that is a routine advance in computing technology, is economic growth. Murphy admits this, but gets hung up on the fact that these other things can not improve. This is a problem, because

As long as these physically-bounded activities comprise a finite portion of our portfolio, no amount of gadget refinement will allow indefinite economic growth. If it did, eventually economic activity would be wholly dominated by us “servicing” each other, and not the physical “stuff.”

To which I say: what is wrong with that? Here is what Murphy thinks is wrong with that, and here we get to what may be his fundamental error:

The important result is that trying to maintain a growth economy in a world of tapering raw energy growth (perhaps accompanied by leveling population) and diminishing gains from efficiency improvements would require the “other” category of activity to eventually dominate the economy. This would mean that an increasingly small fraction of economic activity would depend heavily on energy, so that food production, manufacturing, transportation, etc. would be relegated to economic insignificance. Activities like selling and buying existing houses, financial transactions, innovations (including new ways to move money around), fashion, and psychotherapy will be effectively all that’s left. Consequently, the price of food, energy, and manufacturing would drop to negligible levels relative to the fluffy stuff. And is this realistic—that a vital resource at its physical limit gets arbitrarily cheap? Bizarre.

This scenario has many problems. For instance, if food production shrinks to 1% of our economy, while staying at a comparable absolute scale as it is today (we must eat, after all), then food is effectively very cheap relative to the paychecks that let us enjoy the fruits of the broader economy. This would mean that farmers’ wages would sink far lower than they are today relative to other members of society, so they could not enjoy the innovations and improvements the rest of us can pay for.

The first paragraph simply lacks imagination, but the second one is almost unforgivable. Food production has already gone from being nearly 100% of the economy to a much smaller proportion of it. Are farmers poorer as a result? Of course not. There are fewer of them and each one produces food for more people. This is how food has got cheaper in the first place. A human body needs 100 Watts to work. We could completely automate food production using some multiple of 100 Watts per person which is only a small proportion of each person’s energy budget, and there is your almost free food. With this kind of material abundance economic activity can be completely intellectual, no problem at all.

Can growth continue forever after that? It is possible that we will hit some limit of how much computation, and therefore intellectual activity, can be done with the available energy. Ray Kurzweil has tried to calculate the physical limits of computation and his answers are in units of how many entire civilisations can be simulated per second. So the limits are quite high.

This is Murphy’s other error. He writes, “I am unsettled by my growing concerns about the viability of our future”. In response to these concerns he proposes abandoning growth, not having kids and not eating meat. But he has gone the wrong way. He calculates that there are limits and is afraid of attempting to reach them. If you flip the argument around, what physics tells us is just how much wealth is possible. I have already described how material abundance can be had for very little energy. There is plenty of energy for a much larger population to live a much longer life with no material concerns and as much entertainment and intellectual stimulation as a person could want. Perhaps Murphy knows this, and it is the source of his cognitive dissonance when he writes, “such worrying is not consistent with who I am.”

…to the UK’s anti-capitalist left in a truly splendid rant:

The callous capitalist west is happy to house you if you want to be housed. It will educate for free from 3 to18 years. It will attend to your medical needs, cradle to grave, regardless of what you do to your own body. It agrees to protect you from hostile countries with a military and from hostile fellow citizens with a police force, whether or not you yourself are a criminal. If you catch on fire it will send someone round to put you out. It will have a justice system to ensure you are fairly treated and will provide a lawyer for you if you need one.

The state doesn’t care what religion you are. What you call yourself. What you wear or where you travel. The state will provide infrastructure every citizen may use regardless of how much taxation that individual has contributed to its development. Anyone may use terminal 5 or New Street station or the M25. It will give you money every week and ask only that you sign for it once every month. More money if you’re ill. Or if its cold.

When you’re sixty five or sixty eight it will give you more money if you have never saved or earned any any of your own.

It won’t even ask you what you’re doing with the cash. It will let you spend it on cigarettes, booze, Cheesy Whatsits, gambling or an E Harmony subscription. The state doesn’t care.

It won’t demand you serve in the military or a national service labour scheme. It doesn’t even ask you to give blood or take part in medical experiments. Or sweep up the streets or even just sign an agreement that you promise only to say nice things about the government.

And that’s just a democratic government. Capitalism adds choice. Technology. Medical advances. Communications. Longevity. Energy. Transportation. Travel. Comfort.

The whole of civilisation has been a struggle to secure enough food to eat and enough shelter to survive.

That’s the argument. The last line stands on its own: what the Wolf-Klein-Monbiot corner sees as the wicked selfishness of trade and the terrible vulgarity occaisioned by choice and freedom, are medicine, not sickness. Read the whole thing here. (H-T: Worstall)

We are often told, even by so-called “left libertarians” who claim to be in favour of markets but not corporatism, that modern corporations, with their evil limited liability protections, favours from the state and so on, can roll over a democratic government and shaft the general public. Up to a point, Lord Copper. In fact, the situation is far more complicated. Some firms seem remarkably weak when confronted with some pressures, which makes me wonder why Hollywood movies still insist on portraying corporate executives as flinty-eyed, heartless bastards on the take. (The irony is, of course, that some of the most ruthless corporations are in the film business).

As evidence, Brendan O’Neill has this excellent piece in the Telegraph about Tesco’s, workfare, and the influence of the “Twitterati”:

“What could be worse than the government’s workfare programme?”, almost every columnist in the land is currently asking. I can think of one thing worse: the awesome and terrifying power of the commentariat and its slavish groupies amongst the Twitterati to strike down initiatives like workfare and almost any other government project that they don’t like. That’s the real story here. Forget the historically illiterate wailing about young people being forced into “slave labour” or the idea that getting yoof to work in return for money is the Worst Thing Ever. The ins and outs of workfare itself pale into insignificance when compared with the new power of tiny cliques of cut-off people to override public opinion and reshape modern Britain.

The speed with which first Tesco, that supposedly arrogant monolith of the high street, and then others withdrew from the workfare scheme was alarming. It was a testament both to the sheepishness of modern corporations (remember this next time someone starts banging on about “free-market fundamentalism”) and to the authority of the therapeutic, suspicious-of-wealth, pro-state, anti-big-business sections of the well-fed media classes, who can now put powerful institutions on the spot simply by penning a few ill-thought-through articles with the word “SLAVE” in them.

One possible quibble: has this not been the case for decades, even centuries? Consider that the opinion-forming classes have tended to be concentrated in the London area, have tended to have an influence out of all proportion to their numbers? This is hardly new. What has changed, clearly, is that in the age of the internet, the speed with which this class can make its voice heard accelerates.

I always thought it was a bit optimistic to imagine that blogging, the internet and so on would massively shift the balance of forces in terms of who gets to influence debate in a country like the UK. The mainstream media still carries big influence, especially television. And our political class, drawn as it is from a relatively shallow pool of talent, is as susceptible to the influence of such opinions as it ever was. However, what I think has changed for the better is that more of us, such as O’Neill and so on, can attack the conventional wisdom through the medium of the internet rather than hope that our letters get printed in some corner of a newspaper.

There is also more of what we might call a “swarm effect” these days with certain issues; I think the internet definitely magnifies this phenomenon. Another consequence is that memory of certain events gets ever shorter as the news cycle spins faster and faster. The Singularity is near!!!.

Update: Guido Fawkes has a delicious twist on this whole business about “workfare” – it involves the Guardian.

“Nothing more poignantly reflects the collapse of the great global warming scare than the decision of the Chicago Carbon Exchange, the largest in the world, to stop trading in “carbon” – buying and selling the right of businesses to continue emitting CO2. A few years back, when the climate scare was still at its height, and it seemed the world might agree the Copenhagen Treaty and the US Congress might pass a “cap and trade” bill, it was claimed that the Chicago Exchange would be at the centre of a global market worth $10 trillion a year, and that “carbon” would be among the most valuable commodities on earth, worth more per ton than most metals. Today, after the collapse of Copenhagen and the cap and trade bill, the carbon price, at five cents a ton, is as low as it can get without being worthless.”

– Christopher Booker

Last night I went to the cinema, which I rarely do nowadays, and judging by the size of the audience for the movie that I and my friend saw, not many other people go to the cinema these days either. The place, in the heart of the London West End, was damn near deserted, apart from us and about three other people. Actually, though, the problem was probably the movie we were seeing, as I will now explain.

The movie we saw was Margin Call. Here is a short Rolling Stone review of it, which strikes me as pretty much on the money.

Okay: SPOILER ALERT. Stop reading this very soon if you don’t want the broad outlines of the plot handed to you on a plate.

When I started watching it, I knew nothing about Margin Call other than that a friend of the friend I was with had said it was the best current financial crisis movie he knew of. This makes sense. Margin Call is very much a trader’s eye view of the moment when the first of the waste matter started to move seriously towards the fan, around 2008. And, remarkable to relate, it actually shows “capitalism” (the quotes being because we all here know how government-intervened-in all these sorts of market have been) in a by no means wholly bad light. I am not a bit surprised now to have learned, the morning after, that this movie was written and directed by an ex-trader, a certain J. C. Chandor.

Plot approaching. Final warning. → Continue reading: What capitalism does when the music stops

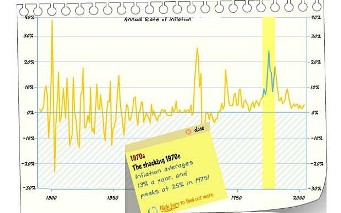

I was struck by this graphic, produced by the money printers at the Bank of England and reproduced in the Telegraph:

We are told (not least by the Bank of England) that deflation is the greatest threat to our well-being. But look at the Nineteenth Century. There’s no end of deflation there. And yet in this time they managed to build almost all of Britain’s railways (including three routes from London to Manchester), the Great Eastern, Crystal Palace, most of London, bring clean water and sewerage to the cities, introduce street lighting, make huge advances in science and medicine. and establish just about all the industries (coal, shipbuilding, steel etc) whose loss is so lamented, especially by people on the left.

OK, so I suspect a lot of those industries would have closed anyway but I fail to see how anyone could look at this graph and honestly claim that deflation was something to fear.

PS I now notice that the BoE does indeed talk about “Years of Deflation” between 1921 and 1931 and my understanding is that it was a pretty grim time. I would be interested to know if there’s a response to the implied claim that deflation is or was a bad thing.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|