We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

Well, things seem a bit quiet around here today, so here is something I photoed earlier:

I encountered the tie at an IEA event about road pricing. The tie proclaims the fact of and the principles espoused by the Mont Pelerin Society. It was being worn by Dr Eamonn Butler, Director and co-founder of the Adam Smith Institute, and, among many other distinguished things, the author of many fine books explicating and popularising the ideas of freedom and of the free market.

One thing puzzles me, though, and my limited googling abilities were unable to solve the puzzle for me. What was so special about the year 1824? That’s an Italian flag, right? So what happened in Italy that the Mont Pelerin Society regards as so worthy of commendation?

I would have asked Eamonn Butler, but my camera has better eyesight than me, and I only saw the 1824 references when I got home.

Following the Rothbard talk I mentioned yesterday, here is another performance by a dead great guy, in this case Milton Friedman, supplied by Sam Bowman at the ASI blog.

What a shame, as Rothbard so regularly noted, that Friedman didn’t include banking in his list of big businesses that the government should not be giving money and power to.

I say dead. Thanks to their books, but now especially thanks to video and audio, and to the internet that now allows us all to choose what video and audio we will pay attention to, these great men live on.

In a posting at Libertarian Home, Richard Carey quotes the late, great Murray Rothbard criticising Keynes. (And while I’m linking to Carey, see also this recent piece about libertarianism by Carey, which is very fine.)

Better yet, Carey also supplies, as a mere comment added later to the Rothbard posting, a recording of a talk by Rothbard, in which Rothbard also lays into Keynes, way back in April 1989. The talk begins with these words:

First of all I want to launch a pre-emptive strike against any critics who might accuse this talk of being ad hominem. The ad hominem fallacy is that instead of attacking the doctrine of a person you attack the person, and that is fallacious because that doesn’t refute the argument. I’ve never been in favour of that. I’ve always been in favour of refuting the doctrine and then going on to attack the person.

And the talk ends (and yes I did listen also to everything in between) with these words.

To sum up Keynes: arrogant, sadistic, power besotted bully, a deliberate and systemic liar, intellectually irresponsible, an opponent of principle, in favour of short-term hedonism and a nihilistic opponent of bourgeois morality in all of its areas, a hater of thrift and savings, someone who wanted to liquidate and exterminate the creditor class, an imperialist, an anti-semite and a fascist. Outside of that, I guess he was a great guy.

Good knockabout stuff, then, and I greatly enjoyed it, despite the occasional pauses where Rothbard rootles around in his papers for his next bit of dirt. The performance lasts about forty minutes.

But be clear that this is Rothbard in attack dog mode, not Rothbard the magisterial expounder of Austrianism. He surveys Keynes’s career and character, and he does whatever is the opposite of cherry picking. With regard to Keynes’s “will to power” and general belligerence towards anyone he disapproved of, I got more than a whiff of the feeling that it takes one to know one, so to speak. Rothbard had plenty of will to power himself, even if he never got a fraction as much of it as Keynes had from the start. In addition to his great theoretical works, Rothbard spent much of his life flailing about trying to build rather unconvincing political alliances, so that he could get some power, but it never worked.

But give Rothbard time. Keynes wielded huge power in the short run, the short run being, as Rothard explains, the thing that Keynes cared about far more than he did about the long run. But I think it is at least reasonable to hope that in the longer run, say in about a hundred years time, Rothbard may be held in far higher esteem than Keynes. For Keynes also did more than his fair share of flailing, in his failed attempts at serious thinking about economics. If, in the long run, Keynes eventually becomes famous only for being utterly wrong, it would be the perfect posthumous punishment for him.

If, on the other hand, Keynes is still held in high esteem in centuries to come, then heaven help the human species. We are in for very bad times.

Besides which, I think that Rothbard is basically spot on, not only about the character and career of Keynes, but about the need for at least some of us to get nasty about such things. One of the signs that the Cold War was ending was when anti-Marxists started getting serious about what an immoral piece of shit Karl Marx was. Marx did not “mean well”. He yearned for social catastrophe of a sort that he knew would kill millions. He was not just wrong in the intellectual sense, he was wrong morally. He promised his Grand Theory of Everything, failed to produce it, but pretended for the rest of his life that he had produced it. This was not just a great mistake and a great folly. It was morally wrong, because intellectually corrupt. It was a Big Lie.

Similar things can be said of Keynes, and Rothbard says them. Good for him.

The problem I often see in left-libertarian writing is the sense that the world of freed markets would look dramatically different from what we have. For example, would large corporations like Walmart exist in a freed market? Left-libertarians are quick to argue no, pointing to the various ways in which the state explicitly and implicitly subsidizes them (e.g., eminent domain, tax breaks, an interstate highway system, and others). They are correct in pointing to those subsidies, and I certainly agree with them that the state should not be favoring particular firms or types of firms. However, to use that as evidence that the overall size of firms in a freed market would be smaller seems to be quite a leap. There are still substantial economies of scale in play here and even if firms had to bear the full costs of, say, finding a new location or transporting goods, I am skeptical that it would significantly dent those advantages. It often feels that desire to make common cause with leftist criticisms of large corporations, leads left-libertarians to say “oh yes, freed markets are the path to eliminating those guys.” Again, I am not so sure. The gains from operating at that scale, especially with consumer basics, are quite real, as are the benefits to consumers.

– Steve Horwitz.

(Hat/Tip, Econlog, which has other thoughts here.)

I am all in favour of ending “corporate welfare” – for ALL sizes of firms; I think tariffs, subsidies, “soft loans”, eminent domain property land-grabs, huge extensions to intellectual property such as patents (I think some forms of IP are okay, the more clearly and narrowly defined), and so on, count as such welfare. But none of this means we have to make the error of automatically saying that small firms are somehow less bad than larger ones are. And remember that when a firm, even a brilliantly-run one with no government aid, gets large, that unless it is very lucky, its sheer size can reduce its nimbleness in responding to new challenges to its position. I don’t have the data to hand, but I read somewhere that of the firms in the Dow Jones Industrial Average in 1950, fewer than half are still there.

So the next time you hear someone waxing indignant about WalMart or Tesco’s, bear that sort of thing in mind.

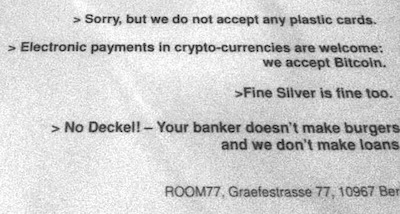

I would recommend clicking on the picture for the large version, in order to read the house policy of the establishment for the use of firearms on the premises.

My apologies for the poor quality of the picture. The light was dim, and I merely had a phone camera. I could have stolen the menu in order to get a better picture, I suppose, but I would not dream of violating the property rights of people of such obvious soundness.

Keynesian policies will keep us in a constant loop of distorted markets and growing imbalances. They guarantee us a Groundhog Day of economic depression.

— Detlev Schlichter, 8th November 2012

…triple-dip recession…

— The Bank of England, 14th November 2012

“Nobody pretends that hiking these taxes means “ordinary people” will have less tax to pay. But most folk still believe that companies can be made to pay taxes, shifting the burden away from the rest of us. I have news for you: they can’t. Corporations are artificial legal constructs: only people can ever pay taxes. The burden of taxes supposedly levied on companies is borne either by investors (through reduced returns on their capital), workers (via lower wages) or consumers (as a result of higher prices). Targeting firms is just a way of stealthily taxing these people, ensuring nobody really understands who is picking up the bill. It is because we’ve forgotten about these basic principles that we’ve ended up with a dysfunctional and incomprehensible tax system, as exemplified by the row over the practices of Starbucks, Amazon, Google and others.”

Allister Heath. (Non-UK residents who don’t subscribe may not be able to see the full Telegraph article, but it seems that quite a lot can, so I am putting this up with a disclaimer.)

A year ago today I posted Discussion Point XXXVI

What will happen to the Euro? I am not asking “what should happen”, but what will happen. Take this opportunity to put your predictions on the internet, and later be hailed as a true prophet or derided as a false one.

Come, take your bows, or your lumps, and predict anew. The fat lady has not yet sung.

Assuming that global warming really is happening, and really is caused by man, the rich will get off nearly scot free, as usual.

Ain’t that great!

The reason that it truly is good news for all humanity is that, whereas we have scarcely an inkling as to how to stop global warming, and our efforts to change human behaviour so as to mitigate it show an unbroken record of failure in all aspects save that of making new pretexts for tyranny, we do now know how to end poverty.

Hell, we’ve done it, in the rich world. Clue’s in the name.

If you are poor in the rich world, and are annoyed at me for saying this, do feel free to write in and complain. Email in, I mean, on your personal computer using your broadband connection or the one provided for free in a public library.

Hell, we’ve got halfway to doing it in great swathes of what was once the poor world. Last month I read about some Parisian hotel developer who caused outrage when he said his exclusive new hotel wouldn’t be open to Chinese tourists. Then he backtracked in a hurry and said “he was referring to ‘mass tourism’ when he used the phrase ‘Chinese tourists’.” Yes, I know hundreds of millions of Chinese are still poor, but think of how far we have come when a snob thinks of the Chinese when he denigrates ‘mass tourism’. Think of how far we have come when the outrage is expressed by Chinese internet users.

Hell, but hell on earth is getting less hellish by the day. There is harder evidence for this than my little anecdote above. Look up worldwide life expectancy statistics. This despite the mad folly of the economic policy of practically every government in the world. We have got so stonkingly, gobsmackingly, tingle-down-your-leggingly good at poverty reduction over the last few decades that we can even do it with socialism round our necks. Just think what we could achieve without that millstone.

We could exterminate the poor as a class. Would that not be agreeable? Quote me on that, you global warming activists who divide your time between Copenhagen and New York; I find the poor tiresome and would rather not have them around any more. I’d rather have all the Chinese, and all the Indians, and all the Africans getting rich and flying to London to take pictures of each other in front of London landmarks, in rotation if need be. It might cause a bit of global warming. Never mind, we rich folk can live with that.

Here:

The gold you see in the photo above was not found in a river or a mine. It was produced by a bacteria that, according to researchers at Michigan State University, can survive in extreme toxic environments and create 24-karat gold nuggets. Pure gold.

Maybe this critter can save us all from the global economic crisis?

On the contrary, this is not the dream, it is the nightmare. This bug, if it really can “create” 24-karat gold nuggets, or can in the future be persuaded to, might destroy gold as a meaningful replacement for the deranged fiat currencies now ruining all out lives.

A commenter tries to reassure us about the cost of this process, but his misspelling of “affect” does not inspire me with much confidence:

This is cost-prohibitive on a large scale, so it would/could not really effect the gold market.

Well maybe for a while, but technology these days is notoriously prone to plunge in cost with the passing of time.

The good news is that this bug doesn’t, like a government creating fiat money, create gold out of thin air. It creates it out of gold chloride. I presume that gold chloride is very roughly as rare as gold itself, as in similar order of magnitude rare. Heaven help the global economy if it is not rare. According to this Gizmodo piece, gold chloride costs “Less than gold, but still plenty”. Please, make it so.

As to the future, please, let no very large stashes of gold or gold chloride be found on nearby planets or asteroids.

Thank you Instapundit. Or not as the case may be.

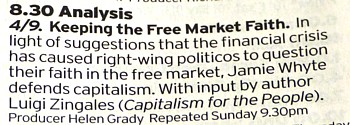

Incoming from Jamie Whyte:

I have made a programme for Analysis on BBC Radio 4 which will be broadcast on Monday at 8.30pm. It concerns the Conservatives’ wrong headed abandonment of free markets following the financial crisis. You won’t learn anything you don’t already know — but then you are not the target audience! Nevertheless, you may be amazed to hear these things said on the BBC.

Relevant bit of the Radio Times (Monday October 8th):

Internet info from the BBC:

The financial crisis has made many on the political right question their faith in free market capitalism. Jamie Whyte is unaffected by such doubts. The financial crisis, he argues, was caused by too much state interference and an unhealthy collusion between government and corporate power.

Indeed.

I’m now watching a video of Hans Sennholz, produced by the Foundation for Economic Education.

Sennholz is talking about the Great Depression, arguing that freedom didn’t fail, politics failed, and that “if we repeat these government polices there is going to be another Great Depression”. I’m typing while he talks, but that is the gist of it.

Until now, Sennholz was just a name to me. Now he is a name, a face, a voice, an attitude. And a prophet.

This video was made (or should I say this film was shot?) on February 29th (!) 1988. I was steered towards it by Richard Carey (whom I SQotDed earlier this week) of Libertarian Home, to whom thanks.

The First World War use to be called The Great War. Soon, The Great Depression is likely also to become known by a different title, which also includes the word “First”.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|