We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

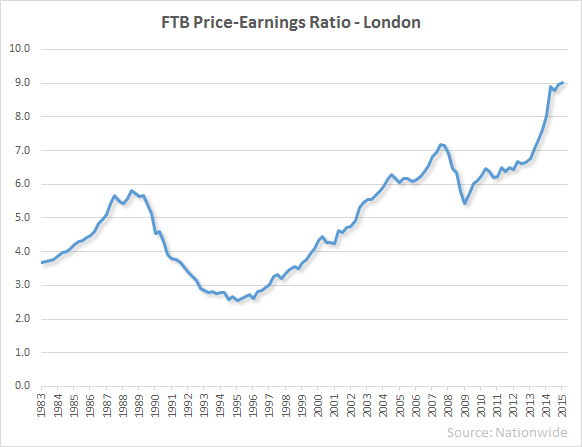

This is not going to end well (Part 38,239) This was tweeted by Dominic Frisby earlier today:

As he says: “1st-time-buyer earnings-to-house-price ratio in London. Gulp. And London 1st-time-buyers are old too … ”

The moment interest rates go up, even slightly, there is going to be an almighty collapse.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|

Yes Sir – the property market is a bubble, and the stock market is also a bubble. All created by the credit-money expansion.

However, this is not just a British thing – most countries are like this.

As for when it will collapse – I thought it would collapse years ago.

The tragically underestimated the fanatical zeal and determination of the international establishment elite.

They have shown themselves prepared to do anything, anything at all, to keep the credit bubble going.

They either do not know or do not care about the twisting of the capital structure of the various economies.

Actually we can all relax now – as it is now impossible to do anything constructive, the damage has been done.

We have run off the high cliff (far off) there is no point screaming or throwing one’s arms about.

Time to relax – and die.

The above should read “I tragically underestimated” not “The tragically underestimated”.

But we are not subject to economic law, we have a Central Bank…

Rising house prices indicate rising prosperity…

Rising house prices are good for investor optimism and ‘animal spirits’…

Inheritance tax is good for the economy as it spreads wealth around…

Deflation is bad, I hate things getting cheaper, in fact, if they do, I’ll stop buying anything as I have an infinite time preference…

A National Debt doubling in 5 years is nothing to worry about, we owe it to ourselves…

On a more cheerful note for 1st time home buyers (or 20-30 year mortgage holders as it were)

The price of houses in Detroit Mi., and Fergeson Mo. in the US have become “unexpectedly affordable”.

Goodness, Capt., why don’t I set up my modest homestead in Detroit (yecch) or Ferguson.

Actually the Mayor of Detroit appears to have at least heard of the concept of Reality. I understand he’s in favor of an armed populace. Good gad!

I’m not sure interest rates will have much effect: my Dad’s place in EW1 went on the market last year, 11 of the 12 people who looked were Chinese cash buyers.

“I thought it would collapse years ago.”

But Paul, it did collapse years ago. It’s just that the Federal Reserve (along with all other major central banks) flooded the market with cash to re-inflate the bubble. And now our bank regulators (and the government-sponsored mortgage agencies, Fannie Mae and Freddie Mac) are pushing to eliminate down payments and permit no-equity loans to borrowers with ever-lower credit quality. One would think that we would remember the lessons of the collapse of 2008, but not only have we forgotten them, we never learned them in the first place. Our grandparents learned a few lessons during the Great Depression, which they carried with them for all of their lives. We, on the other hand, are apparently incapable of learning even from our own mistakes, let alone those of others.

In the US in 2012, interest (just the interest, not any principal repayments) on the national debt amounted to almost 15% of total tax revenues. That’s with the Fed grossly manipulating the capital markets to keep interest rates at essentially zero. Imagine what those numbers will look like when (as is inevitable) interest rates rise to more historically normal levels. Of course this is not going to end well.

And that’s especially true now that the Chinese (with the assistance of many of our nominal allies, including England, Germany and France) is busily setting up an Asian Infrastructure Investment Bank to compete with the World Bank and the International Monetary Fund. Once that becomes fully operational the dollar’s status as the world’s reserve currency will be severely weakened, the dollar’s artificial strength will vanish, and the whole structure of western finance will be irrevocably altered (and not to the benefit of the US or, I think, the rest of the west). This will end very badly indeed except, perhaps, for the Chinese, although I don’t think even they fully understand the extent of their own financial weakness or the damage they will suffer with a dollar collapse.

It is for this reason that I cannot see interest rates being allowed to rise. The state is a huge borrower, and its so-called independent central bank sets the interest rate. These are probably the end days of this scam, but that does not mean that they cannot keep it going for a long time.

Massive misallocation of capital due to too much cheap money floating around the system. Sounds like a lot of folk are about to learn that house prices go down as well as up and also that actions have consequences.

Cry me a river.

Hypotheses must be specific in order to be falsifiable. Writing that a collapse will occur at *some* point is not specific enough to be falsifiable.

Laird writes that a collapse has already occurred – in 2008 – but that the bubble was reinflated. Yet the downstream consequences of that collapse were limited; there was no hyperinflation of consumer prices for example. Why does this episode not count as a falsification of the Austrian hypothesis? And what reason is there to think that a future collapse cannot also be averted by similar means of “reinflation”?

It occurs to me that I may have got slightly over-alarmed when I wrote this. Firstly, price-to-earnings ratio is not the same as mortgage-to-earnings ratio which will be lower. Secondly, (and Frisby implies this) there aren’t as many first-time buyers these days.

Still bad though, just not quite as bad.

I have absolutely no evidence to support my guess, but I think the bubble will only burst in 2018 at the earliest, and 2020 at the latest. I remember there were economic crises in 1986, 1997, and 2008. Going on this trend, it seems the next one should hit in 2019.

Have the Austrians managed to explain why it often occurs in ten-eleven year cycles?

Mike, this isn’t the place for an extended discussion of hyperinflation, etc. However, there are two short answers to your question (I can only speak to the US):

The first has to do with the velocity of money. The Fed has been paying banks not to lend (it pays them interest on “excess reserves”, which was illegal prior to 2008), and as a consequence a huge amount of dollars has been sequestered in Fed deposits (see this graph). If (when) the banks begin lending again those dollars will start leaking out into the economy which, exacerbated by our system of fractional reserve lending, will trigger massive inflation. Not necessarily hyperinflation (economists have a specific definition of that term) but at least significant inflation.

Second, since the dollar is presently the world’s reserve currency, and the US is viewed as the strongest economy around, foreign institutions are significant buyers of dollars. Foreign central banks hold large reserves of them, and other institutional investors view Treasurys as the safest place to park extra cash. This has the effect of sopping up a lot of excess dollars and keeping interest rates unusually low. No other country enjoys this advantage. But once it ends (this relates back to the last paragraph in my previous comment), and the dollar becomes subject to all the same market forces as are other currencies, many of those dollars will come flooding out, again triggering significant (measured) dollar inflation. Sooner or later we will have to pay the piper, which is pretty much what Patrick’s post is about.

It will keep going as long as wealth (as different from tokens/money) can be stolen from somewhere to keep the bubble inflated.

That theft seems to be being hidden remarkably well at the moment – inflation is so low.

Quite strange.

Perhaps its that blacky-golden light before the massive storm hits?

I sincerely hope not.

I owe better to my children.

Some countries have not had major home price corrections: Australia and Canada to name two of them. UK house prices are not too crazy, but London attracts all the money from the corrupt countries: 1) The 57 odd Muslims Countries 2) The dictatorship countries of Asia and Africa.

In the US Miami housing is crazy because every Latin American with money has a place there to keep at least some of it away from the Caudillos, Marxist crazies in Venezuela, Argentina, Brazil, Ecuador and Bolivia and so forth. The Central Americans buy in the US and Panama.

As far as the sovereign debt crisis, The Wobbly Guy, may have it right. I would watch Japan, France, the Club Med countries as well as the emerging market countries that have $9 trillion in US denominated debt (mostly corporate debt not sovereign). If our FED raises rates (and there will be more than one rate rise as there was in 1937)there will be some very bad things happening down the road.

Paul Marks:

In fairness to their point of view, they are at least consistent: They believe that they can, and should, manipulate all markets to produce better-than-free-market outcomes. The interest-rate market is just one more, from their point of view.

John Galt III:

Canada has had fewer artificial incentives than the U.S., in the real estate market. We do have government mortgage insurance, but nothing else in the way of inducements to buy a house, other than interest rates controlled by a central bank. Even there, rates have historically been a percent or so above U.S. rates (for reasons not related to the housing market). Also, probably mainly for geographic reasons, Canada’s high real estate prices are confined to a few cities — mainly Vancouver, Calgary, and Toronto. Elsewhere in Canada real estate remains fairly affordable, and booms generally only occur when some other kind of economic activity is a factor (such as the booms and busts in Edmonton related to the oil industry).

Tedd,

I know the Calgary market very well as I travel there a lot. If oil stays around $50 for 2 years, Calgary will get crushed. China’s misallocation of capital will eventually hurt the Chinese a great deal and there goes Vancouver. If China dries up its growth and oil stays low, Toronto will suffer as Canada’s balance of trade and balance of payments goes negative and the Canadian economists calling for a drop of 30-50% in Canada home prices will finally be correct. The consumer debt per capita in Canada is insane.

Quebec and Ontario have a worse provincial debt problem than California has a state debt problem and California is in seriously bad shape. The Fraser Institute of BC has written many papers on this and I have read each one carefully.

Love going to Alberta and just made a week’s reservation there for mid-June, but Canada has some serious problems and these problems will manifest themselves shortly.

Wobbles, the sun-spot cycle is about 11 years in length. Nobody yet knows why.

John Galt III:

You misunderstood my purpose. It was merely to explain the past and present state of affairs. I’m aware that Canada is not immune from the laws of nature, and that other problems exist (a very low and dropping savings rate, for example).

What is interesting is that there is a huge housing bubble, and stock market bubble, caused by money inflation (printing) – but there is no rise in other prices, such as consumer prices or commodities. Can somebody explain this?

Thank you Laird, but it seems to me that given the interventions that central banks and governments may make in the event of a crisis, it is not clear how Austrian claims about the business cycle can be falsified.

mike what is your point about falsification? Is it relevant to economics? There is the Robinson Crusoe model, but you cannot do experiments in economics without e.g. Killing millions as socialists seem to start off doing with guns, then by starvation (it saves ammo).

@Mr Ed

Sure. Without falsifiability, there is limited predictive value. Since the subject is financial collapse with its attendent consequences of inflation and so on, I think that’s a rather important thing to predict.

mike,

I think that the thrust of economics is that it is based not on scientific falsification but logic deduction from premises. People are not atoms that have predictable properties in the manner of chlorine and caesium but they do tend to act in economic terms in manners driven by value. It all starts with supply and demand, and distortions to supply of money. However, just as no man steps in the same river twice, as the saying goes, no day’s economic data is the same as the previous day usw.

Well ok. But then there isn’t much to say beyond 1) at some unspecified point there will be inflation and other consequences, and 2) we should return to limited government and sound money. But note that 2) does not require the support of Austrian business cycle theoryand can instead be claimed on other grounds.

So if Austrian business cycle theory is to be useful it has to be in prediction. Otherwise it’s just talk.

mike, it might be useful if you are an entrepreneur and wish to be the first into the wave of money (and not the one holding the parcel of IOUs when the music stops). And in any event, if it is correct, whether or not it is useful is neither here nor there, it would be truth for its own sake.

A weather forecast is more useful to my farmer neighbours than it is to me, but if it is accurate, it is still something to appreciate.

Well truth for its’ own sake is great if you can be confident you aren’t in error, or you haven’t missed something, which was the concern behind Popper’s falsification criterion.

I’m not saying that Austrian business cycle theory is wrong, I am merely pointing out that its lack of predictive power means that even if it is right you can’t use it to do anything that you couldn’t have been doing already.

Predictive power is great, mike, but so is explanatory power. And the Austrian theory does a very good job (far better than any other) of explaining business cycles and economic events over the last century or so. Moreover, the fact that it doesn’t give you a fixed date for, say, the next financial collapse doesn’t mean that it isn’t predictive, merely that it is not as precise in its predictions as you would like. That doesn’t make it invalid, let alone useless.

Falsification is a useful tool for scientific theories, but economics isn’t science. You can dress it up all you like with sigmas and deltas and other greek letters, and with superscripts, subscripts and numbers on their sides, but in the end economics is only applied human psychology. As Mr Ed already noted, people aren’t atoms, and they aren’t subject to statistical forecasting (which is why Hari Seldon was wrong). All one can reasonably expect from any economic theory is correlations, directions and trends. When you start believing the hype of “scientific” economists, who have the hubris to claim the ability to effectively micromanage a nation’s economy, you have entered the world of fantasy. But that is precisely where your desire for “prediction” takes you.