We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

Instapundit linked yesterday to a fascinating little Slashdot titbit about the price of digital books. Apparently, a crime writer called John Locke has lowered the price of his latest book from around what a book book costs to make and distribute, to a price much nearer to what an eBook costs to write and distribute, that is to say, he has dropped his price by about ninety percent. And he has been doing far better with this new arrangement than he did with the old one.

‘These days the buying public looks at a $9.95 eBook and pauses. It’s not an automatic sale,’ says Locke. ‘And the reason it’s not is because the buyer knows when an eBook is priced ten times higher than it has to be. And so the buyer pauses.

I certainly pause. For as long as eBooks cost the same as books, then I will prefer books, because I am used to books and eBooks are like … well, I don’t know what they’re like exactly, and at ten quid a go or whatever, I can’t be bothered to find out. But when eBooks start costing a tenth of what books cost, that is to say, less even than remaindered or second-hand books, then I’ll probably do a rethink.

Since writing the above, I have discovered that quite a few commenters on the Slashdot piece are of the exact same mind as me about eBooks.

It all reminds me earily of the early price of DVDs, which I recall as one of the oddest episodes in recent techno-biz history. For a fleeting little moment, DVDs were priced according to a “logic” that said that, since DVDs enable you to watch a movie lots of times over, that means that the proper price for a DVD is several times the price of a cinema ticket. Seriously, they thought they could get away with charging about forty quid for the things. Which, by the way, explains the ridiculously elaborate cases that individual DVDs still typically get sold in. When DVDs started out, they thought they were selling something almost unimaginable in its luxuriousness. They thought they were selling an even better version of those enormous metallic discs that they used to sell at about a hundred quid a pop to millionaires of the sort who really did have real home cinemas. Which they sort of were. But that didn’t mean that the rest of us were willing to pay millionaire money to get our hands on a decent DVD collection. We could already guess what DVDs cost to make (not a lot) and until we saw that fact reflected in the prices we were being asked to pay, we sat on our hands.

And that is what has surely been going on during the last year or two with eBooks. They haven’t charged for eBooks like they were hardbacks, but they have looked at what they consider to be the added convenience when deciding about price, rather than looking at the cost to them of making and distributing the product and the consequent opportunity to reach a whole new raft of customers with a dramatically reduced price. A few pioneers willing to pay off the development costs of the new gizmos have paid for these early eBooks. But now, eBooks will surely plummet in price, just as DVDs did.

Occasionally people tell me that I should write a book. I’m pretty sure that will never happen, but the eBook phenomenon, which I sense is about to get truly phenomenal (both in how books are read and in how they are created), may change my mind about that.

When I wish to buy cheap low end computer accessories (cables, card readers, laptop batteries, etc), I find that it is much cheaper to buy them on eBay from foreign sellers, rather than from anyone in the UK. I have been doing this for five years or more, and it is interesting to see where the items then come from. Five years ago, they were almost always from Hong Kong, with return addresses in places like Yuen Long. (“The unfashionable end of the western spiral arm of the New Territories”). The markets where the sellers get them from are actually over the border in Shenzhen in China proper, so I suspect that these sellers make regular trips to the markets over the border, bring stuff back, and then post it to buyers in the West.

I still get items from Hong Kong, but in recent times it has become more common for then to come from Shenzhen. I am not sure if this is due to another set of eBay sellers having come into being on the other side of the border, or if the same ones are simply posting from a post office on the other side of the border because this is cheaper. (How international postal services relate to one another, and whether and how much money is paid from the sender to the recipient national post office is a complete mystery to me, alas. I suspect it is as baroque as the equivalent system of international telephone call settlements (which I did understand) was before it collapsed under its own insanity. There are undoubtedly some hidden and probably unintentional subsidies somewhere here). My hunch is, “a little of both”. Some Hong Kong sellers posting in Shenzhen – some Shenzhen sellers.

In recent times, the items have occasionally been posted from Dongguan, part of essentially the same economic and manufacturing cluster as Shenzhen (although not a Special Economic Zone, but politically speaking just an ordinary prefecture level city in Guangdong province). However, far enough away from Hong Kong that Hong Kong people are not going to go there to buy and send stuff. Therefore, these sellers are definitely mainland Chinese.

And today, I received an item from Zhangpu in Fujian province, a good way north up the coast. This is one of the more prosperous regions of coastal China (south of the Special Economic Zone in Xiamen), but Hokkien rather than Cantonese speaking and far from recent European influence and probably a centre more for trade and investment from also Hokkien speaking Taiwan. It is interesting to see this sort of activity moving up the coast, but there is no sign of it moving inland. Of course, it is always going to be close to the factories.

However, write a little English, and the fact that you can sell stuff to people throughout at least the English speaking world has clearly been learned. As an observation, I have found such Chinese sellers to be reliable and honest in their dealings with me. They send you exactly what they say, the products all work properly, and if there is any kind of problem (such as a missing item due to postal problems) they are eager to resolve it. An excellent eBay reputation is very important to such people. This works so well that I don’t actually bother looking at eBay feedback from Chinese sellers before buying: I simply assume that the system has weeded unreliable and dishonest sellers out automatically.

On the other hand, this particular purchase was a card reader, for which I paid a total of £1.67. including postage. eBay fees might amount to about 20p. The postage label says that postage cost ¥9.60, which is at present equal to about 90p. This leaves about 57p to pay for the card reader. Allowing the seller a modest 17p profit, we are left with a card reader coming out of the factory no more than 40p (and possibly a good deal less, depending on how many middle men there are), which is a miniscule sum of money.

My preferred conclusion from this is that economies of scale are wonderful, capitalism is grand, and modern technology is awesome, in that technological products all become so cheap so fast that almost nobody has to be excluded from owning them. And this is true, of course, although I worry about something else. When capital is too cheap due to excessively easy credit, all kinds of capital intensive businesses appear to be profitable, when in reality they are receiving a subsidy from the banking system. (Another, non-Chinese example: a large portion of Europe-Asia air travel has in recent years been taken over by airlines based in the Middle East Gulf states. The cost of capital of these airlines is artificially low, as they are implicitly backed by the oil wealth of Abu Dhabi. Whether they would be profitable with out this, it’s hard to tell).

China’s banking system is incredibly opaque. The bits that we can see aren’t especially pleasant to look at. And of course, opaque = bad, pretty much by definition. When everything unwinds, the consequences will be unpleasant, featuring scenarios that will appear oddly familiar to us. Government bailouts of banks, savers being robbed of the value of their savings, and inflation, perhaps. And perhaps this is already happening. £1.67 is actually a bit on the high side, compared to prices I was paying for similar items a few months back.

Here is a good piece by Rob Fisher about the latest episode of Channel 4 TV’s 10 O’clock Live. Particularly good bit:

Another highlight was the interview with Stephen Dubner, a co-author of SuperFreakonomics. The interviewers Jimmy Carr and Lauren Laverne failed to say anything remotely intelligent, but it thankfully didn’t matter too much because they did at least let Dubner speak at length. He made some good (and downright subversive) points about the incentives of politicians. He suggested that they sign up for long term projects such as “improve education” and they get paid at the end of 5 or 10 years proportional to the results. The idea is to align success in politics with success at achieving goals, and he compared this to how businesses succeed and fail. Getting this kind of thinking into the mainstream – not necessarily agreeing with the specifics but just getting people to think about economics and game theory and how politics really works – is great stuff. Well done Dubner and Channel 4.

I agree with Rob. My preferred attitude to spreading ideas has always been to unbundle them, to try to spread them, at any rate in hostile circumstances, one at a time or at least only a very few at a time. Bundling among friends is also, if you think about it, often saying just the one thing or just the few things, that the bundling of this with that and maybe also with that makes sense – this, that and that having already been long agreed about separately.

I haven’t watched 10 O’clock Live beyond episode one, but applaud Rob for doing so. We need our people everywhere, and watching (between us) everything.

“Today we are coming to realize that our land is finite, while our population is growing. The uses to which our generation puts the land can either expand or severely limit the choices our children will have. The time has come when we must accept the idea that none of us has a right to abuse the land, and that on the contrary society as a whole has a legitimate interest in proper land use. There is a national interest in effective land use planning across the nation.”

This piece of communitarian nonsense was issued by a senior US politician in the 20th Century (I quote from page 11 of “Property Rights and Eminent Domain” by Ellen Frankel Paul).

I wonder if Samizdata readers can guess who said these words. Some might be quite surprised, some not.

Update: answer – Richard Nixon.

“There was never any widespread popular demand for change, and the argument that people would find a decimal system easier was true in practice only of those who rarely used it, i.e., foreigners. From an educational point of view, our duodecimal system was preferable because it taught children how to count in different bases. People brought up before decimalisation are almost invariably better at mental arithmetic than those born since. When we lost our shillings and pence, as when, more gradually, our weights and measures were subverted, we lost the full meaning of many of our nursery rhymes, jokes and proverbs. We also lost the actual coins, all of them superior in design to what replaced them and all, because they remained in circulation so long (it was common in the 1960s to receive a Victorian penny in change), of historical interest. Indeed, this is literally true, since the inflation of the Heath/Wilson years made the new coins almost valueless.”

Charles Moore, Spectator, page 11, 19 February edition (behind the subscriber firewall).

He is right on this. Yes, I can see some readers sniffing that a lot of old rot about rhymes and so on is hardly any reason for keeping a form of coinage, but I think he has a point about different bases in counting; even in my own field of finance and banking, I noticed that in some areas, such as the pricing of US bond securities, the practice was recently, or still is, to mark prices in sixteenths and 32nds, rather than in the decimal form used for Eurozone bonds, for example. And being able to do this is good for my maths – not a strong point.

But the broader issue surely, is that while the loss of old coinage may be upsetting to traditionalists, the real nub of the matter is that there is no point in embracing some “modern” standard of counting or whatever if the government, and central bank, debauches the currency. And unfortunately, even during the “good old days” when old coinage existed, the quackery of inflationism was eroding the value of those pounds (a unit of weight, remember) and everything else. I would settle for any coinage system so long as it retained its value.

What killed respect and affection for money was not the decimalisation mania of the late, unlamented Sir Edward Heath. It was inflation.

I sometimes pick up quick-to-read paperbacks, either fiction or non-fiction, at airports to help pass the time during my flight. So, on a recent short break to Malta, I bought Dambisa Moyo’s How the West Was Lost, published a short while ago, which seeks to argue that for various reasons, good and bad, the West (essentially, Western Europe and North America) is in danger of losing out to the East. I was intrigued enough to pay a few quid for the book, but in the end I should have known better.

Moyo has a lot of things to say with which free marketeers might approve of: she denounces the way in which the banking system has encouraged over-use of debt financing, creating all manner of problems, culminating in the sub-prime mortgage disaster and associated asset price bubble; she also understands that modern Welfare States have created many problems. However, for all that she tries to accept that the rise of the former Third World nations from poverty is a Good Thing and to be applauded, I cannot help but feel that she does not really mean it very much. She’s a mercantilist who sees economics as a titanic fight between states and is hostile, or at least sceptical, about the capacity of people operating in markets under the rule of law. And she repeats the canard that the panic of 2008 demonstrated the dangers of unfettered capitalism, oblivious to the fact that the monetary policies of the Fed, etc, were policies of state institutions, as was the interference in the US and other housing markets by governments (Freddie Mac, etc).

In fact, she seems wedded to a sort of neo-Malthusian argument that says that the desire for prosperity and higher living standards in places such as China is unmitigated bad news for the West as there are finite resources in energy, etc, and that Eastern prosperity comes at the expense of the West’s. In other words, she is arguing that economics is, in some ways, a case of winners and losers. Indeed, she talks repeatedly about the idea of there being a race, often using the very word… “race”… to make her points.

Here is one typical paragraph in which she says the West is suffering from all that terrible selfish individualism and we should benefit from a bit more of that no-nonsense collectivism as seen in China (page 172):

“Frankly speaking, the constitutional framework that has defined the US for the past three centuries is not likely to be amended in order to hand over more power to the state. Yet arguably more power, more flexibility and fewer committees are exactly what is needed. What sense does it make in the depths of the financial crisis – a state of economic emergency by most accounts, which brought the country and the world to its knees – for the President of the United States to have to build consensus around a desperately needed fiscal stimulus package before he and his advisors can act?”

She seems curiously unaware of to what extent the powers of the Federal government in the US have already gone way beyond what was envisaged by the Founders – and that’s a bad thing – and that in other Western nations, such as the UK, the government of the day has considerable powers, or has yielded great powers to the European Union and its legions of unelected officials. And yet for Ms Moyo the problem is that is far too much of this pesky liberalism, checks and balances, and so forth. I hate to say it, but she’s coming close to flirting with a form of fascism.

There are other, equally poor, arguments. For instance, she argues that the vast majority of citizens in Western nations have only reaped a small share of the benefits of greater trade and so on because many of the profits earned are paid to shareholders. For instance: (page 178) “The only thing companies were interested in was the company’s profitability and therefore the shareholders’ return on capital.”

Wow, the owners of firms want to make a profit (as opposed to making a whacking great loss, presumably). But even this line ignores the fact that by “shareholder”, we do not just mean a few isolated fat, capitalist bastards in suits; no, we also mean all the millions of people – including people a bit like Ms Moyo – who have savings plans, 401K plans, mutual funds, pension pots, etc. This line of hers also does rather beg the question of what should happen to these profits – should they be taxed in “reinvested” by governments? In several instances, she praises the behaviour of governments, such as oil-rich states, and their massive “sovereign wealth funds”, arguing that these are used to benefit domestic populations. Well they may be in some cases, but even a cursory awareness of public choice economics should alert Ms Moyo to the dangers of corruption, mis-allocation of capital, political favouritism and faddism that often comes when government agencies disburse vast sums. The flashy public spending projects of the past have often brought dubious rewards.

And I just knew I had wasted my aircraft reading time when she scorned Ricardo’s Law of Comparative Advantage, arguing that unless all countries play “fair” (which never happens), then the argument for free trade that the LCA underpins is chucked away.

This argument – that free trade is only beneficial if everyone plays nice – has been demolished time and again. A good example comes from Deepak Lal, in his book, Reviving the Invisible Hand.

Here is a passage:

“a country will benefit from removing its own tariffs and import restrictions even if all its trading partners maintain theirs. For as long as the domestic prices of goods in our country under autarky differ from those at which they can be imported and exported under free trade, the country will be able to obtain the gains from trade both by obtaining imported goods at a lower cost than they are produced at home (the consumption gain) and by specialising in producing and exporting those goods in which it has a comparative advantage and importing the others (the production gain), irrespective of the tariff applied by their trading partners. For these trade restrictions only damage the protectionist country’s welfare, and it would be senseless not to improve one’s own welfare just because someone else is damaging theirs. There is no point throwing rocks into one’s harbour just because others are throwing rocks into theirs. Hence, there is an incontrovertible case for every country to unilaterally adopt free trade, irrespective of the protectionist policies of other countries – with one exception. Suppose that a country is the only producer of some good – say, oil.”

He goes on to explain this case but says that in fact, retaliatory trade practices and other issues take the edge off this argument also.

It is all such a pity. She started well, but I really wish I had read that new Lee Child thriller instead.

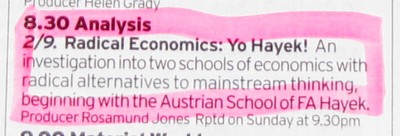

As in BBC Radio 4, this coming Monday, January 31st, 8.30 pm:

That’s from the current Radio Times. As you can tell from the pink, I will be paying close attention. My thanks to fellow Samizdatista Chris Cooper for alerting me to this radio programme.

But will it be an attempt at a hatchet job? It seems not:

This week, Jamie Whyte looks at the free market Austrian School of F A Hayek. The global recession has revived interest in this area of economics which many experts and politicians had believed dead and gone. “Austrian” economists focus not on the bust but on the boom that came before it. At the heart of their argument is that low interest rates sent out the wrong signals to investors, causing them to borrow to spend on “malinvestments”, such as overpriced housing. The solution is not for government to fill the gap which private money has now left. Markets work better, Austrians believe, if left alone. Analysis asks how these libertarian economists interpret the state we’re in and why they’re back in fashion. Is it time to reassess one of the defining periods of economic history? Consensus would have it that the Great Depression of the 1930s was brought to an end by Franklin D Roosevelt’s Keynesian policies. But is that right? Jamie Whyte asks whether we’d all have got better quicker with a strong dose of Austrian medicine and whether the same applies now?

I think I first encountered Jamie Whyte at a Cobden Centre dinner.

I was disappointed with the recent Robert Peston TV show about the banking crisis, despite appearances on it by Toby Baxendale, the founder of and Chairman of the Cobden Centre. All the fault of the banks was the basic message, with governments looking on helplessly. No mention (that I can now recall) of those same governments monopolising the supply of money and relentlessly determining the price of borrowing it, all day and every day, all the time.

But, my understanding of Baxendale and of the Cobden Centre is that he (it) is playing a long game, giving broadcasters whatever they ask for (in Peston’s case Baxendale messing about with fish), while all the time asking them to give the Cobden Centre’s ideas at least something resembling a decent hearing. Don’t compromise on the ideas, but be endlessly mellow and accommodating at the personal level, intellectual steel in velvet glove, and so on and so forth. If that’s right, then it may be starting to work.

John Hawkins: Now, in recent years we started to hear more people calling to get rid of the Federal Reserve. Good idea, bad idea? What are your thoughts?

Thomas Sowell: Good idea.

John Hawkins: Good idea? What do you think we should replace it with? What do you think we should do?

Thomas Sowell: Well it’s like when you remove a cancer what do you replace it with?

Indeed. And not just the price of all the other kinds of gas.

Am I the only one who suspects that a lot of the climate change hubbub whipped up in recent years was really just a cover for getting young lefty-inclined scientists to find other kinds of energy, not actually to save the planet, but rather to enable the rulers of the West to tell those pesky Arabs to take a hike? I don’t read the right sort of blogs and websites to know for sure, but I doubt very much that I am.

Anyway, now, another kind of energy has come on stream, of the sort that conflicts with all the climate change hubbub, because it is disturbingly similar in its imaginary climatic effects to the stuff that our rulers want to be able to stop buying from the Arabs.

The BBC’s Roger Harrabin quotes the Chief Economist at the International Energy Association, Dr Fatih Birol:

“There’s suddenly much more gas available in the world than previously thought,” he told BBC News.

“It’s cheaper than it was and the supply is more assured. And it’s only half as polluting as coal. There will be strong debates between energy and climate and finance ministries round the world about whether investment should continue to support renewables when the situation on gas has so radically changed.”

That settled science is already turning out to be not so settled after all, and this just might be part of the reason, don’t you think? Governments, for their own reasons that have nothing to do with the actual argument, are now switching from being climate change fanatics to what the climate change fanatics call climate change deniers.

The moral is: if you want to spread some ideas, any ideas, don’t rely on governments to help you. They will help you, if and while it suits them. But if and when it stops suiting them, you’d better be ready to win your argument all by your little old self.

The other night, when I had the TV on, I saw that one of the programmes, featuring the BBC top economics and business correspondent, Robert Peston, was all about the financial panic of recent years. Oh dear, I thought, I can just imagine the usual line about how it was all the fault of greedy bankers, insufficient regulation, “unregulated laissez faire capitalism”, and on and on. Well, not quite. Yes, some of those elements were there, but there was also quite a lot of sophisticated explanation of how a combination of forces – leverage, “too big to fail bailout protection, over-confidence in newfangled ideas of risk management and misalignment of incentives for bankers – combined to create the storm. I would have liked to see more focus on the role of ultra-low central bank interest rates in creating the crisis, as well as government intervention in the housing market and through deposit insurance, but to be fair, this was mentioned, several times. There was little in the show with which someone like Kevin Dowd, recently referred to here, would dispute, although I imagine Kevin might want to make more about the vexed issue of ownership of banks and limited liability.

And about three-quarters of the way into the show was Toby Baxendale, founder of the Cobden Centre, the organisation founded last year to flag up the problems caused by central banking fiat money, and which sets out alternative ideas, such as the possibility of giving depositors in no-notice cash accounts the right to demand that their cash is properly looked after, not lent out for months in a risky play. (Yup, it is that pesky fractional reserve banking issue again). Toby was very forceful and his views were treated respectfully by Peston. There was no sneering.

In short, this was and is a pretty good programme as far as the MSM goes. I give it about 8 out of 10. Yes, I am not drunk.

“If you wanted to fly and there were no supervisory authority in the airline industry and no regulations enforcing safety standards, you would be very reluctant to fly fledgling airlines. You would prefer the established ones that had the track record and the reputation. So a complete lack of safety regulations in the airline industry would favour established firms, making the entry of new ones impossible and killing competition and consumer choice.”

Raghuram G. Rajan and Luigi Zingales, from page X (in the Roman numeral segment) of “Saving Capitalism from the Capitalists.” Published in 2003.

This is an interesting defence of government-imposed safety standards. I am not wholly convinced by this line of argument; it is, for sure, an interesting way of trying to show how government regulation actually stimulates rather than restricts entry into a particular line of business.

My take is that if a fledgling airline, say “Ultra-Cheap Airlines Inc.,” can persuade investors and others to get it started in business with a few aircraft and so on, then the staff on the aircraft – such as the pilots – will not set foot into an aircraft if they fear that safety has been compromised, or if the aircraft are poorly maintained. Pilots are not usually self-destructive, as far as I can tell. In fact, a debutant airline business would bend over backwards to show customers that it had set high standards, get consumer watchdog organisations and other certification providers to give it a “seal of approval”. What the authors of the quote don’t seem to understand is how the “established” airlines got to be in that positions in the first place. Presumably, they had to start by persuading a highly nervous customer base that flight was safe, or at least, not lethal.

And of course, if the standards imposed by regulators are particularly onerous, then it is hard to see how a small business operating a few aircraft could afford to compete with the big boys. Regulations are a form of barrier to entry, much in the same way that extensive licensing of doctors is designed, quite deliberately, to regulate the number of people working as physicians.

This book is generally pretty good, however; it is interesting to read this book alongside the Martin Hutchinson/Kevin Dowd book about financial markets that I quoted the other day.

I know, my friends, that you are concerned about corporate power. So am I. So are many of my free-market economist colleagues. We simply believe, and we think history is on our side, that the best check against corporate power is the competitve marketplace and the power of the consumer dollar (framed, of course, by legal prohibitions on force and fraud). Competition plays mean, nasty corporations off against each other in a contest to serve us. Yes, they still have power, but its negative effects are lessened. It is when corporations can use the state to rig the rules in their favor that the negative effects of their power become magnified, precisely because it has the force of the state behind it. The current mess shows this as well as anything ever has, once you realize just what a large role the state played. If you really want to reduce the power of corporations, don’t give them access to the state by expanding the state’s regulatory powers. That’s precisely what they want, as the current battle over the $700 billion booty amply demonstrates.

This is why so many of us committed to free markets oppose the bailout. It is yet another example of the long history of the private sector attempting to enrich itself via the state. When it does so, there are no benefits to the rest of us, unlike what happens when firms try to get rich in a competitive market. Moreover, these same firms benefited enormously from the regulatory interventions they supported and that harmed so many of us. The eventual bursting of the bubble and their subsequent losses are, to many of us, their just desserts for rigging the game and eventually getting caught. To reward them again for their rigging of the game is not just morally unconscionable, it is very bad econonmic policy, given that it sends a message to other would-be riggers that they too will get rewarded for wreaking havoc on the US economy. There will be short-term pain if we don’t bailout these firms, but that is the hangover price we pay for 15 years or more of binge lending. The proposed bailout cannot prevent the pain of the hangover; it can only conceal it by shifting and dispersing it among the taxpayers and an economy weakened by the borrowing, taxing, and/or inflation needed to pay for that $700 billion. Better we should take our short-term pain straight up and clean out the mistakes of our binge and then get back to the business of free markets without creating an unchecked Executive branch monstrosity trying to “save” those who profited most from the binge and harming innocent taxpayers in the process.

What I ask of you my friends on the left is to not only continue to work with us to oppose this or any similar bailout, but to consider carefully whether you really want to entrust the same entity who is the predominant cause of this crisis with the power to attempt to cure it. New regulatory powers may look like the solution, but that’s what people said when the CRA was passed, or when Fannie and Freddie were given new mandates. And the very firms who are going to be regulated will be first in line to determine how those regulations get written and enforced. You can bet which way that game is going to get rigged.

I know you are tempted to think that the problems with these regulations are the fault of the individuals doing the regulating. If only, you think, Obama can win and we can clean out the corrupt Republicans and put ethical, well-meaning folks in place. Think again. For one thing, almost every government intervention at the root of this crisis took place with a Democratic president or a Democratic-controlled Congress in place. Even when the Republicans controlled Congress, President Clinton worked around it to change the rules to allow Fannie and Freddie into the higher-risk loan market. My point here is not to pin the blame for the current crisis on the Democrats. That blame goes around equally. My point is that hoping that having the “right people” in power will avoid these problems is both naive and historically blind. As much as corporate interests were relevant, they were aided and abetted, if unintentionally, by well-meaning attempts by basically good people to do good things.The problem is that there were a large number of undesirable unintended consequences, most of which were predictable and predicted. It doesn’t matter which party is captaining the ship: regulations come with unintended consequences and will always tend to be captured by the private interests with the most at stake. And history is full of cases where those with a moral or ideological agenda find themselves in political fellowship with those whose material interests are on the line, even if the two groups are usually on opposite sides.

– Professor Steven G. Horwitz, writing in late September 2008, in a piece entitled An Open Letter to my Friends on the Left. This evening, Horwitz will be giving a talk at the Institute of Economic Affairs in London, entitled An Austrian Perspective on the Great Recession 2008-2009.

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|