We are developing the social individualist meta-context for the future. From the very serious to the extremely frivolous... lets see what is on the mind of the Samizdata people.

Samizdata, derived from Samizdat /n. - a system of clandestine publication of banned literature in the USSR [Russ.,= self-publishing house]

|

This person at the Daily Caller appears – with some justification I might add – to take a dim view of Ron Paul, the US congressman and Republican primary contender for the presidential ticket known as “Dr No” on account of his saying no to various government measures and enterprises. He is, famously or infamously, a hardline anti-interventionist in foreign affairs, so much so that his views might be dubbed as almost pacifist. He has called for accountability by the Federal Reserve, and argues that institution ought to be closed down. But he has feet of clay, and this article I link to, which is written in a sort of furious burst of anger, focuses on those flaws and makes light of Paul’s merits. In particular, the article unfairly misrepresents the Austrian school of economics and its methodology. It also seems to smear libertarianism on issues like legalising prostitution and drugs, ignoring the obvious arguments that criminalising consensual acts has created huge costs for society.

All the way down at the bottom of a comment thread prompted by this article, is large item by commenter Michael P. Ivy. It is so good that I reproduce it here. There is the odd typo, but it is worth quoting in the raw:

I am always amused by wannabe economists, who call themselves capitalists, but, are unable to embrace or understand the true axioms of capitalism when push comes to shove. Austrian economics spins on essentially to axioms: (1) that there is no free lunch, and (2) all human action is purposeful action motivated by the individual’s (not society’s) desire to move from a less to a more desired state. These are self evident truths, much like the “more is preferred to less” axiom of the neoclassical school. You butcher Rothbard without understanding his work and particularly his crititique of the neo classical school of wackjob indifference curve analysis and welfare economics. The notion that an individual can be indifferent between two different states of the world without ever actually exercising choice is not a reliable basis for recommending redistribution measures of the Kaldor/Hicks kind. Even Samuelson so much as admitted that it is impossible to derive a social welfare function without making assumptions about the marginal utility of money et al (1951).

The problem with Keynes’ economics, is that it must rob resources from one sector of the economy to furnish another and it consumes resources in the process. Moreover, in doing so, the government does so without the knowledge of the benefits that those resources procure that only those individuals holding those resources…know. This is the problem with any measure of government involvement in economics. That they suffer from fiscal illusion (not my money so it don’t matter) is one thing, but, they effectively create an environment of uncertainty by destroying productive incentives. Incentives do matter after all and I have yet to see the mathematical models of the neo-classicals actually recognize this and quantify them. The fact is, is that you can’t unless you invoke a value judgement of the Keynesian/Samuelson kind.

Welfare economics has never worked and it never will work, for as M. Thatcher so plainly points out, “Socialism is a great idea until you run out of other people’s money”. The statement captures two notions: (1) if their actually was a multiplier effect on GDP from government spending, don’t you think this would be a permanent line item of the government’s income/expense statement?, and (2) the No Free Lunch axiom is underscored by the fact that since government is an unproductive entity that consumes resources for its existence without actually creating anything of value is that eventually the productivity of the market is unable to keep up with and compensate for the unproductive actions of government. True capitalists understand this.

And if you think the market is unable to coordinate itself with respect to defense, innovation, policing of private property, mass transit, health, education, indeed all the things you think we require a central planner for, then you obviously have not bothered to school yourself on the opportunities that can and will present themselves if productive individuals are left alone and allowed to participate. Finally, I see that your article is riddled throughout with incorrect and obnoxious assertions about economic theory presented by Rothbard, Mises et al. (semi-autistic dogmatism). The fact is, is that there is nothing dogmatic about the Austrian school. Its core tenet is that the best production, exchange, and coordination of resources occurs when individuals are left free and unfettered to choose. And by whatever math you might care to invoke, given the level of debt ($16T) incurred by the Welfare State, I’d say you’re pointing the dogmatic finger in the entirely wrong direction. THAT is what is dogmatic….doing the same illogical, nonsensical thing over and over again (at the people’s expense), and expecting a different result every time. So before you decide to write another diatribe on someting you don’t know much about, I’d recommend that you review Rothbard…again, and in particular his piece on “Towards a Reconstruction of Utility and Welfare Economics”. There is nothing dogmatic, hairy scary or offensive about it.

Very good.

Ron Paul is very much a mixed bag, and I would not vote for him, and I am troubled by some of his views. But the fact has to be faced that almost unique in Western politics, he has put forward a classical liberal agenda on certain issues, and done so consistently. And he has managed, despite his age, to touch a lot of young people. There is a lesson here somewhere.

As has been noted before, the disaster of the eurozone is, in the eyes of some policymakers, as much an opportunity for further pan-European empire-building as it is an occasion for shame and embarrassment. This week, Angela Merkel, German Chancellor, and Nicolas Sarkozy (remember him? He’s the one who married one of Mick Jagger’s old flames), came up with this barnstormer of an idea, in the form of a European-style “Tobin tax” and a form of increased economic central government. It has the ring of inevitability about it.

The problem for the UK is that said tax, which has been assailed by the likes of Tim Worstall before, would apply not just to the eurozone, but to the UK, which is not in the euro. And given the relative size of London as a financial centre compared to Paris, Frankfurt or Milan, guess which place takes the biggest relative hit? You guessed: London. Never mind, of course, that banks that can do so will put some of their activities outside the EU, or that the costs of the tax will be borne by savers, borrowers and users of financial services generally, in the form of lower rates of savings interest – already negative in real terms – more expensive costs of hedging forex transactions, and the like. This is what is known as tax incidence. Politicians are not, as we know, in the business of understanding the Law of Unintended Consequences. Indeed, we might even define today’s political class as people who defy this law.

Of course, Cameron, Osborne and others (but not their LibDem allies) will protest about such a tax on London’s financial sector, but look how far such protests got us before concerning sovereign debt bailouts by the UK. And such men have shamefully pandered to such anti-capitalist sentiment in the past, so there is a sort of brute justice if they fail to prevent this latest move now. Such men, of course, have enjoyed the fruits of financial wheeler-dealing when the going was good, such as financing of the Tory party by the likes of Michael Spencer, the founder of derivatives powerhouse ICAP. (As an aside, I see that the odious Vincent Cable, Business Secretary, wants to slap capital gains tax on housing transactions of wealthy properties if the Tories decide to ditch the top 50 per cent rate of income tax. Even a land value tax is better than CGT, although not by very much. There is no such thing as a benign tax.)

Alas, banker bashing has reached such heights of hysteria that some might even try and argue that such a tax on the evils of speculation is a jolly good idea. It pained me to see that even that otherwise fine book on the recent market disaster by Kevin Dowd and Martin Hutchinson, floated the idea.

Allister Heath weighs on the latest eurozone wheeze. He’s unimpressed, not surprisingly.

Update: Here is a twist on the issue of tax incidence and taxes on companies. Milton Friedman is magnificent.

The impact of David Cameron’s spending cuts is so impressive.

Update: To be fair, this particular chart does not give Cameron a lot of time to make a difference, but does anyone think it matters?

With respect to the other countries, my gut feelings are that the Spanish numbers are made up, and at least some of the British and Italian debts are backed by real assets that are worth something to a greater extent than are whatever is supposed to be backing the Greek, Irish, and Spanish debts. The Portuguese numbers are probably somewhere in between in terms of believability. Belgium is a riddle wrapped in a mystery inside an enigma inside something French.

HT Tim Harford

“The global paper standard has lasted 40 years but evidence is accumulating daily that its endgame is now fast approaching. The world economy is caught in a deepening financial crisis caused by excessive levels of debt, severe asset price bubbles and overextended banks—all imbalances that are the direct consequence of four decades of unprecedented fiat money creation, of artificially low interest rates and of “lender-of-last-resort” central banking. Monetary policy today—whether by the U.S. Federal Reserve, the ECB or the Bank of Japan—is not much more than an increasingly desperate attempt to postpone via super-low interest rates and periodic debt monetization the painful but unavoidable liquidation of these imbalances. This will not only ultimately prove futile, but will lead to a complete currency catastrophe if pursued further.”

– Detlev Schlichter, writing in the Wall Street Journal. The fact that he is now gigging at the mighty WSJ is, of itself, a great thing.

Update: today is the 40th anniversary of Richard Nixon’s decision to kill off the link between the dollar and gold, although in reality the old gold standard had been dead for much longer.

Instapundit, whom I revere for his relentless, industrial strength linkage (happy tenth anniversary Professor), has been in the habit, in recent times, of linking to pieces about how Americans are getting ever more disappointed by President Obama. But, as I am sure that Instapundit himself appreciates, the disappointment with Obama coming from Obama’s own former supporters is not because Obama’s preferred economic policies are now correctly understood by those ex-supporters to be disastrously destructive, but rather because Obama seems insufficiently determined and skilful in imposing these policies upon Americans who would prefer relatively sensible economic policies.

Obama’s leftist critics are not disappointed with Obama because they have come, reluctantly and through bitter experience, to share the opinion of his policies held by the Tea Party. Rather are such critics disappointed with Obama because he is not crushing the Tea Party, but instead haggling with them, and doing so, as these critics see it, with insufficient skill and nastiness.

Yes, Obama still seems to believe in the same daft policies that these leftist critics favour. But where is the passionate commitment to folly that he persuaded them he felt when he was getting elected, and that they still yearn for? Perhaps someone else (Hillary Clinton?), with greater energy, industriousness and human warmth, could lead America over the cliff with the proper amount of dash and determination, instead of Obama just leading the herd from somewhere in among it.

One should not, in short, confuse the fact – if fact it be – that President Obama is now being thought by ever more Americans to be doing a bad job, with the claim that all of America is coming to its senses in the matter of what it should do about its current economic woes, or what will happen to it, and to the world, if it does not do what it should do.

Today I learned, from someone who was involved in the making of it, that:

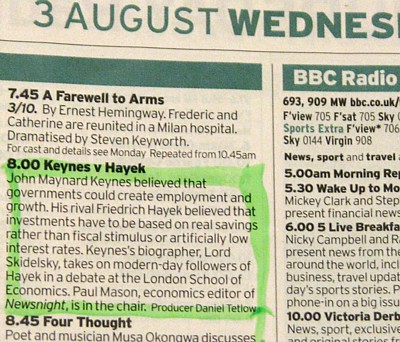

The Radio 4 bosses liked the Keynes v Hayek debate so much that they are going to repeat it at 9 am on Wednesday 24th August. This sort of thing is very very unusual. This is probably going to add around 1.5 million listeners to the estimated 1 million radio listeners the programme has already had. (I haven’t looked at the podcast stats yet but it was in the iTunes News and Politics top 5 in the UK.)

My own personal reaction to the debate was that a true clash of archetypes was too often, for my taste, dragged off into nitpicking about who said what, when, and just what Keynes would have made of Q(antitative) E(asing), when the real point is that he wouldn’t have started from there. But then again, the show was flagged up as “Keynes v Hayek”, rather than as “Mainstream Economics v Austrian Economics”, so I probably shouldn’t grumble but should instead be counting blessings.

Which are numerous. Far more to the point, the above news makes me think, again, more so, this, which said that we are at least, at last, having this argument, beyond the confines of the Austrian Economics tribe and of the tiny few others who had until recently actually heard of it. Austrianism is now emerging from the great gaggle of alternatives to the present disastrous economic policies to take pride of place, at least in the heads of a great many of those who think seriously about economic policy, as The Leading Contender.

This is, in short, very good news, which puts an interesting slant on the ever ongoing argument about whether and how the BBC is biased.

Taking a break from life in riot-torn London, I came across this item at the FT about some of the implications of longer lifespans. It is a mixed situation. Excerpt:

“Maxmin admits there are no miraculous solutions to the problems of a fast-ageing society. We will all have to work longer, save more and pay more in tax to cover the costs of a world with a greyer population. Even so, he thinks models like Elder Power can have a much wider application. Perhaps moments like the collapse of Southern Cross, he tells me, could (in the right hands) become moments of opportunity. More generally, models like Beacon Hill Village, ITNAmerica and Elder Power show glimpses of a future in which more elderly people can stay in their homes for longer. All three use innovative technology, make use of assets in their local community and bring together the resources of local businesses, volunteers and the state to solve problems none could have solved individually, at reasonable cost.”

How we deal with ageing, and the issue of longer lifespans, is of course intertwined with the current fiscal breakdown of many developed economies. Healthcare costs are skyrocketing. And in that Greg Lindsay and John Kasarda book I have been linking to lately, about the impact of mass aviation, there is a segment on how said aviation can be used to dramatically reshape healthcare, such as by flying people with problems to cheaper, but arguably better run, hospitals in Asia. It struck me while reading this book that while automobiles and consumer electronics have been propelled by their Henry Fords, Michael Dells and Steve Jobses, we haven’t really had, in healthcare, a similar set of individuals to drive innovation and push things sharply down the price curve. The dynamics of Silicon Valley, allied with cheap Chinese manufacturing and just-in-time stock inventory systems, hardly touches healthcare at all, although this is starting to change, perhaps. Of course, much of this is caused by how healthcare is seen, wrongly in my view, as somehow “different” from such vulgar things as selling flatscreen TVs or cars. Healthcare is political. That’s the problem.

“The US government has to come to terms with the painful fact that the good old days when it could just borrow its way out of messes of its own making are finally gone” […] In the Xinhua commentary, China scorned the United States for its “debt addiction” and “short sighted” political wrangling. “China, the largest creditor of the world’s sole superpower, has every right now to demand the United States address its structural debt problems and ensure the safety of China’s dollar assets,” it said. It urged the United States to cut military and social welfare expenditure.

– Xinhua News Agency.

No kidding but hey, when a state run by a communist party tells the USA to spend less on… welfare, you start to get some idea just how strange the world has become and just how screwed the US actually is.

“Flowers begin arriving past night and bidding starts before dawn. To ensure their lilies and hyacinths are ready for the auction block, growers move them from cold storage onto carts in the early morning, or else rush them from Schiphol after overnight flights from Quito, Nairobi, and Tel Aviv. It’s impossible to see, much less make sense of, the Aalsmeer at eye level, as the floor of its central warehouse is a thicket of carts bearing blooms, all waiting their turn. This is the world’s largest commercial building at ten million square feet, more than twice the size of Chicago’s Willis Tower or Merchandise Mart….” (Page213).

“From a catwalk running above, you can study the crazy quilt of tulips, sunflowers, azaleas and hydrangeas bleeding into daubs of orange or pink on the horizon. The quilt constantly changes colors and patterns as burly Dutchmen at the wheel of one-man tugs trail daisy chains behind them.” (Page 213)

What is interesting about these passages, concerning the marvels of the vast flower-auction market in Holland, and the global reach of this business made possible now due to aviation and refrigeration, is that the author does not fall into the usual stale bromides about how all this aviation-led trade is killing the planet. I liked this passage, on page 232-3:

“Food miles cannot begin to compare in toxicity with flatulent cattle. Anyone who’s read the Omnivore’s Dilemma can recite chapter and verse on the perils of force-feeding corn to livestock in feedlots. Cows produce methane, a greenhouse gas thirty times more potent than carbon, as a by-product of digestion…..A breakdown of the Big Mac revealed that nearly a third of its [carbon] footprint stems from feed production, another third from storage, and much of the rest from slaughtering, frying, and baking. Food miles contribute 3 per cent.”

Aerotropolis: The Way We’ll Live Next, Greg Lindsay and John Kasarda. 2011.

Tonight,BBC Radio 4, 8pm:

I’m told that it will sound a lot more coherent than it did on the night it was recorded.

More pre-publicity from the BBC here.

American government spending will be higher in 2011 than it was in 2010.

Government spending will be higher in 2012 than it was in 2011 – much higher.

The above is all that matters – everything else is piss and wind.

The deal is one great big shining lie.

– Paul Marks

The first match fixture to be drawn for the 2014 soccer world cup. One of the manifestations of globalization that will go largely unnoticed for a couple of years.

UPDATE: With North Korea and Syria in the same qualifying group of four teams, it looked like we could have a different sort of “Group of Death” than usual, but FIFA chickened out and put Iran and China in other groups.

MORE: Guatemala and Belize. The former’s government claims ownership of the latter. Football correspondent with war zone reporting experience required?

On a more pleasant note, the job I want is covering CONCACAF Group B: Trinidad & Tobago, Guyana, Barbados and the Bahamas. Well, someone has got to go there and report on the beaches, I mean football matches…

EVEN MORE: “In consideration of the delicate political situation between Russia and Georgia, FIFA has agreed to a UEFA request that these two teams not be drawn together.” [From the news feed here]

|

Who Are We? The Samizdata people are a bunch of sinister and heavily armed globalist illuminati who seek to infect the entire world with the values of personal liberty and several property. Amongst our many crimes is a sense of humour and the intermittent use of British spelling.

We are also a varied group made up of social individualists, classical liberals, whigs, libertarians, extropians, futurists, ‘Porcupines’, Karl Popper fetishists, recovering neo-conservatives, crazed Ayn Rand worshipers, over-caffeinated Virginia Postrel devotees, witty Frédéric Bastiat wannabes, cypherpunks, minarchists, kritarchists and wild-eyed anarcho-capitalists from Britain, North America, Australia and Europe.

|